Get instant alerts when news breaks on your stocks. Claim your 1-week free trial to StreetInsider Premium here.

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED

SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-21034

SANFORD C. BERNSTEIN FUND II, INC.

(Exact name of registrant as specified in charter)

1345 Avenue

of the Americas, New York, New York 10105

(Address of principal executive offices) (Zip code)

Joseph J. Mantineo

AllianceBernstein L.P.

1345 Avenue of the Americas

New York, New York 10105

(Name and address of agent for service)

Registrants telephone number, including area code: (800) 221-5672

Date of fiscal year end: September 30, 2022

Date of reporting period: September 30, 2022

Table of Contents

ITEM 1. REPORTS TO STOCKHOLDERS.

Table of Contents

SANFORD C. BERNSTEIN FUND II, INC.

INTERMEDIATE DURATION INSTITUTIONAL PORTFOLIO

ANNUAL REPORT

SEPTEMBER 30, 2022

Table of Contents

Before investing in the Sanford C. Bernstein Fund II, Inc., a prospective investor should consider

carefully the portfolios investment objectives and policies, charges, expenses and risks. These and other matters of importance to prospective investors are contained in the portfolios prospectus, an additional copy of which may be

obtained by visiting our website at www.Bernstein.com and clicking on Investments, found in the footer, then Mutual Fund InformationProspectuses, SAIs and Shareholder Reports or by calling your financial advisor or by

calling Bernsteins mutual fund shareholder help line at 212.756.4097. Please read the prospectus carefully before investing.

For performance

information current to the most recent month-end, please visit our website at www.Bernstein.com and click on Investments, found in the footer, then Mutual Fund InformationMutual Fund Performance at a Glance.

This shareholder report must be preceded or accompanied by the Sanford C. Bernstein Fund II, Inc. prospectus for individuals who are not shareholders of

the Fund.

You may obtain a description of the Funds proxy voting policies and procedures, and information regarding how the Fund voted proxies

relating to portfolio securities during the most recent 12-month period ended June 30, without charge. Simply visit www.AllianceBernstein.com, or go to the Securities and Exchange Commissions

website at www.sec.gov, or call AllianceBernstein at 800.227.4618.

The Fund will file its complete schedule of portfolio holdings with the Commission

for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. The Funds Form N-PORT reports are available on the Commissions website at www.sec.gov.

Investment Products

Offered: · Are Not FDIC Insured · May Lose Value · Are Not Bank Guaranteed

Table of Contents

Portfolio Manager Commentary (Unaudited)

To Our ShareholdersNovember 15, 2022

On the following pages, you will find the 2022 annual report for the Sanford C. Bernstein Fund II, Inc.Intermediate Duration Institutional Portfolio

(the Portfolio). The annual report covers the six- and 12-month periods ended September 30, 2022, and includes financial statements as well as notes to

the financial statements, information about the recent performance of the Portfolio and a listing of the Portfolios holdings as of the period end.

Global equity markets have been challenged over the 12-month period ended September 30, 2022, with most stock

indices down more than 20%, the conventional threshold defining a bear market. In addition, volatility has been elevated throughout most of 2022, marking a turbulent period for investors. Significant economic and geopolitical stress created a tough

macroeconomic backdrop, with both inflation and central banks interest-rate policies coming in higher than the markets anticipated.

One of the

greatest surprises for markets has been the outperformance of the US dollar, which has negatively impacted US companies earnings coming from overseas, while geopolitical forces continue to put pressure on international earnings and economic

growth. In contrast to most of the past decade, value stocks have outperformed growth stocks, but stock selection overall has been challenging. Our equity funds seek to find balanced exposure across factors and the portfolio teams have been pivoting

to companies with strong balance sheets, pricing power and defensive characteristics, while also seeking to capture opportunities due to valuation dislocations.

The pressure on inflation and interest rates has also made the past year one of the worst on record for fixed-income markets. While this has been very

painful for investors, the portfolio teams are leaning into higher yielding issues, with yields notably higher than they were even at the beginning of this calendar year.

Looking ahead, we are carefully minding the odds of recessions in the US and around the world. In this environment, we are confident in our portfolio

teams ability to find the right balance to position for the eventual rebound and the opportunities that are being created today. Thank you for your continued confidence in our approach.

If you have any questions about your investments in the Portfolio, please contact your Bernstein Advisor by calling 212.756.4097, or visit www.Bernstein.com.

As always, we are firmly dedicated to your investment success.

Sincerely,

Onur Erzan

President and Chief Executive Officer

Sanford C. Bernstein Fund II, Inc.

Investment Objectives and Policies

The Portfolio seeks

to provide safety of principal and a moderate to high rate of current income. The Portfolio seeks to maintain an average portfolio quality minimum of A, based on ratings given to the Portfolios securities by any nationally recognized

statistical rating organization (NRSRO) (or, if unrated, determined by AllianceBernstein L.P., the Portfolios investment adviser (the Adviser), to be of comparable quality). Many types of securities may be purchased by

the Portfolio, including corporate bonds, notes, US government and agency securities, asset-backed securities, mortgage-related securities, bank loan debt, preferred stock and inflation-protected securities, as well as others. The Portfolio may also

invest up to 25% of its total assets in fixed-income, non-US dollar denominated foreign securities, and may invest without limit in fixed-income, US dollar denominated foreign securities, in each case in

developed- or emerging-market countries.

The Portfolio may use derivatives, such as options, futures contracts, forward contracts and swaps.

The Portfolio may invest up to 25% of its total assets in fixed-income securities rated below investment-grade (BB or below) by NRSROs (commonly known as

junk bonds). No more than 5% of the Portfolios total assets may be invested in fixed-income securities rated CCC by NRSROs.

In

managing the Portfolio, the Adviser may use interest-rate forecasting to estimate an appropriate level of interest-rate risk at a given time. The Adviser may moderately shorten the average duration of the Portfolio when it expects interest rates to

rise and moderately lengthen average duration when it anticipates that interest rates will fall.

(Portfolio Manager Commentary continued on next page)

|

2022 Annual Report |

1 | |

Table of Contents

Portfolio Manager Commentary (continued)

The Portfolio seeks

to maintain an effective duration of three to seven years under normal market conditions. Duration is a measure that relates the expected price volatility of a security to changes in interest rates. The duration of a debt security is the weighted

average term to maturity, expressed in years, of the present value of all future cash flows, including coupon payments and principal repayments.

The

Adviser selects securities for purchase or sale based on its assessment of the securities risk and return characteristics as well as the securities impact on the overall risk and return characteristics of the Portfolio. In making this

assessment, the Adviser takes into account various factors including the credit quality and sensitivity to interest rates of the securities under consideration and of the Portfolios other holdings.

The Portfolio may enter into foreign currency transactions on a spot (i.e., cash) basis or through the use of derivatives transactions, such as

forward currency exchange contracts, currency futures and options thereon, and options on currencies. An appropriate hedge of currency exposure resulting from the Portfolios securities positions may not be available or cost effective, or the

Adviser may determine not to hedge the positions, possibly even under market conditions where doing so could benefit the Portfolio.

Investment Results

The table on page 8 shows the Portfolios performance compared to its benchmark, the Bloomberg US Aggregate Bond Index, for the six- and 12-month periods ended September 30, 2022. The table also includes the Portfolios peer group, as represented by the Lipper Core Bond Funds Average (the

Lipper Average). Funds in the Lipper Average have generally similar investment objectives to the Portfolio, although some of the funds may have different investment policies, sales and management fees, and fund expenses.

During both periods, the Portfolio underperformed the benchmark and outperformed the Lipper Average. In the 12-month

period, yield-curve positioning was the largest detractor, relative to the benchmark, mostly from overweights to the five- and 10-year parts of the curve that were partially offset by an overweight to the six-month part of the curve and an underweight to the 20-year part of the yield curve. Security selection also detracted, as selection within investment-grade corporate bonds,

asset-backed securities and US agency mortgages outweighed a gain from selection within commercial mortgage-backed securities (CMBS). Sector allocation contributed, due primarily to gains from an underweight to US agency mortgages, an

overweight to asset-backed securities and exposure to US inflation-linked bonds that were greater than losses from allocation to collateralized loan obligations, agency risk-sharing transactions and eurozone high-yield corporate bonds. Currency

decisions also contributed, mainly from short positions in the Swedish krona and offshore Chinese renminbi. Country allocation was a minor contributor to performance during the period.

During the six-month period, security selection within investment-grade corporate bonds and asset-backed securities

was the largest detractor, offset by gains from selection within CMBS. Country allocation to Japan and the UK also detracted, offset partially by allocation to the eurozone. Yield-curve positioning was a minor detractor to performance. Currency

decisions contributed the most to performance, due to short positions in the offshore Chinese renminbi, Australian dollar and Canadian dollar. Sector allocation also contributed, as gains from an underweight to US agency mortgages, an overweight to

asset-backed securities and exposure to US inflation-linked bonds were larger than a loss from exposure to collateralized mortgage obligations and agency risk-sharing transactions.

During both periods, the Portfolio utilized derivatives in the form of interest rate swaps and futures to manage and hedge duration risk and/or to take

active yield-curve positioning. Currency forwards were used to hedge foreign currency exposure and to take active currency risk. Inflation swaps were used to hedge inflation and for investment purposes to incorporate the Portfolios Investment

Management Teams view on future inflation in the Portfolio. Credit default swaps were utilized to hedge credit risk and as a tool to effectively gain exposure to specific sectors. The utilization of government-agency-related To Be Announced

mortgage positions was a significant contributor to the Portfolios turnover rate of 129%.

Market Review and Investment Strategy

During the 12-month period ended September 30, 2022, fixed-income government bond market yields increased

rapidly, and bond prices fell in all developed markets. Most major central banks aggressively tightened monetary policy by raising short-term interest rates and ending bond purchases to combat high and persistent inflation. Developed-market

government bonds fell the most in the UK and eurozone, and by the least in Japan. In credit risk sectors, securitized assets generally outperformed corporate bonds. Investment-grade corporate bonds trailed

(Portfolio Manager Commentary continued on next page)

| 2 |

Sanford C. Bernstein Fund II, Inc. |

|

Table of Contents

Portfolio Manager Commentary (continued)

treasuries,

underperforming in the US against US Treasuries, while outperforming in the eurozone relative to eurozone treasuries. High-yield corporate bonds trailed in the US versus US Treasuries while eurozone high yield outperformed eurozone treasuries.

Investment-grade emerging-market corporate bonds slightly trailed developed-market corporates.

Longer-maturity emerging-market sovereign bonds

underperformed developed-market treasuries. Emerging-market local-currency bonds lagged as the US dollar advanced against almost all developed- and emerging-market currencies. Brent crude oil prices ended the period higher, even as prices fell

sharply in the final quarter on global growth concerns and reduced demand.

|

2022 Annual Report |

3 | |

Table of Contents

Disclosures and Risks (Unaudited)

Benchmark Disclosures

None of the following indices or averages reflects fees and expenses associated with the active management of a mutual fund portfolio. The Bloomberg

US Aggregate Bond Index represents the performance of securities within the US investment-grade fixed-rate bond market, with index components for government and corporate securities, mortgage pass-through securities, asset-backed securities and

CMBS. The Lipper Core Bond Funds Average is the equal-weighted average returns of the portfolios in the relevant Lipper Inc. category; the average portfolios in a category may differ in composition from the Portfolio. The Lipper Core Bond Funds

Average contains portfolios that invest primarily in investment-grade debt issues (rated in the top four grades) with dollar-weighted average maturities of five to ten years. An investor cannot invest directly in an index or average, and their

results are not indicative of the performance for any specific investment, including the Portfolio.

A Word About Risk

The share price of the Portfolio will fluctuate and you may lose money. There is no guarantee that the Portfolio will achieve its investment objective.

Cybersecurity Risk: As the use of the internet and other technologies has become more prevalent in the course of business, the Portfolio has become

more susceptible to operational and financial risks associated with cybersecurity. Cybersecurity incidents can result from deliberate attacks such as gaining unauthorized access to digital systems (e.g., through hacking or

malicious software coding) for purposes of misappropriating assets or sensitive information, corrupting data, or causing operational disruption, or from unintentional events, such as the inadvertent release of confidential information. Cybersecurity

failures or breaches of the Portfolio or its service providers or the issuers of securities in which the Portfolio invests have the ability to cause disruptions and impact business operations, potentially resulting in financial losses, the inability

of Portfolio shareholders to transact business, violations of applicable privacy and other laws, regulatory fines, penalties, reputational damage, reimbursement or other compensation costs, and/or additional compliance costs. While measures have

been developed which are designed to reduce the risks associated with cybersecurity, there is no guarantee that those measures will be effective, particularly since the Portfolio does not control the cybersecurity defenses or plans of its service

providers, financial intermediaries and companies in which it invests or with which they do business.

Cybersecurity incidents, both intentional and

unintentional, may allow an unauthorized party to gain access to Portfolio or shareholder assets, Portfolio or customer data (including private shareholder information), or proprietary information, or cause a Portfolio, the Adviser, and/or the

Portfolios service providers (including, but not limited to, fund accountants, custodians, sub-custodians, transfer agents and financial intermediaries) to suffer data breaches, data corruption or lose

operational functionality, or prevent Portfolio investors from purchasing, redeeming or exchanging shares or receiving distributions. A Portfolio and the Adviser have limited ability to prevent or mitigate cybersecurity incidents affecting

third-party service providers. Cybersecurity incidents may result in financial losses to such Portfolio and its shareholders, and substantial costs may be incurred in order to prevent any future cybersecurity incidents.

Interest-Rate Risk: Changes in interest rates will affect the value of investments in fixed-income securities. When interest rates rise, the value of

existing investments in fixed-income securities tends to fall and this decrease in value may not be offset by higher income from new investments. Interest-rate risk is generally greater for fixed-income securities with longer maturities or

durations. The Portfolio may be subject to greater risk of rising interest rates than would normally be the case due to the end of a recent period of historically low rates and the effect of potential government fiscal and monetary policy

initiatives and resulting market reaction to those initiatives.

Credit Risk: This is the risk that the issuer or the guarantor of a debt

security, or the counterparty to a derivatives or other contract, will be unable or unwilling to make timely principal and/or interest payments, or to otherwise honor its obligations. The issuer or guarantor may default, potentially causing a loss

of the full principal amount of a security and accrued interest. The degree of risk for a particular security may be reflected in its credit rating. The credit rating of a fixed-income security may be downgraded after purchase, which may adversely

affect the value of the security. Investments in fixed-income securities with lower ratings tend to have a higher probability that an issuer will default or fail to meet its payment obligations, making credit risk greater for medium-quality and

lower-rated debt securities. Lower-rated debt securities and similar unrated securities (commonly known as junk bonds) have speculative elements or are predominantly speculative credit risks. At times when credit risk is perceived to be

(Disclosures and Risks continued on next page)

| 4 |

Sanford C. Bernstein Fund II, Inc. |

|

Table of Contents

Disclosures and Risks (continued)

greater, credit

spreads (i.e., the difference between the yields on lower quality securities and the yields on higher quality securities) may get larger or widen. As a result, the values of the lower quality securities may go down

more and they may become harder to sell.

Duration Risk: The duration of a fixed-income security may be shorter than or equal to full maturity of

the fixed-income security. Fixed-income securities with longer durations have more interest-rate risk and will decrease in price as interest rates rise. Securities that have final maturities longer than their durations may be affected by increased

credit spreads to a far greater degree than their durations would suggest, because they are exposed to credit risk until final maturity.

Inflation

Risk: This is the risk that the value of assets or income from investments will be less in the future as inflation decreases the value of money. As inflation increases, the value of the Portfolios assets can decline as can the value of the

Portfolios distributions. This risk is significantly greater for fixed-income securities with longer maturities. Rates of inflation have recently risen, which could adversely affect economies and markets.

Inflation-Protected Securities Risk: The terms of inflation-protected securities provide for the coupon and/or maturity value to be adjusted based on

changes in an inflation index. Decreases in the inflation rate or in investors expectations about inflation could cause these securities to underperform non-inflation-adjusted securities on a

total-return basis. In addition, there can be no assurance that the relevant inflation index will accurately measure the rate of inflation, in which case the securities may not work as intended. These securities may be more difficult to trade or

dispose of than other types of securities.

Foreign (Non-US) Securities Risk: Investments in foreign

securities entail significant risks in addition to those customarily associated with investing in securities such as less liquid, less transparent, less regulated and more volatile markets. These risks include risks related to unfavorable or

unsuccessful government actions, reduction of government or central bank support, inadequate accounting standards and auditing and financial recordkeeping requirements, lack of information, and adverse market, economic, political and regulatory

factors and social instability, all of which could disrupt the financial markets in which the Portfolio invests and adversely affect the value of the Portfolios assets.

Emerging-Markets Securities Risk: The risks of investing in foreign (non-US) securities are heightened with

respect to issuers in emerging-market countries because the markets are less developed and less liquid and there may be a greater amount of economic, political and social uncertainty, and these risks are even more pronounced in frontier

markets, which are investable markets with lower total market capitalization and liquidity than the more developed emerging markets. Emerging markets typically have fewer medical and economic resources than more developed countries, and thus they

may be less able to control or mitigate the effects of a pandemic. In addition, the value of the Portfolios investments may decline because of factors such as unfavorable or unsuccessful government actions and reduction of government or

central bank support.

Derivatives Risk: The Portfolio may use derivatives as direct investments to earn income, enhance return and broaden

portfolio diversification, which entail greater risk than if used solely for hedging purposes. In addition to other risks such as the credit risk of the counterparty, derivatives involve the risk that changes in the value of the derivative may not

correlate with relevant assets, rates or indices. Derivatives may be difficult to price or unwind, and small changes may produce disproportionate losses for the Portfolio. Certain derivatives have the potential for unlimited loss, regardless of the

size of the initial investment. Assets required to be set aside or posted to cover or secure derivatives positions may themselves go down in value, and these collateral and other requirements may limit investment flexibility. Some derivatives

involve leverage, which can make the Portfolio more volatile and can compound other risks. Derivatives, especially over-the-counter derivatives, are also subject to

counterparty risk, which is the risk that the counterparty (the party on the other side of the transaction) on a derivative transaction will be unable or unwilling to honor its contractual obligations to the Portfolio. Use of derivatives may have

different tax consequences for the Portfolio than an investment in the underlying asset or index, and such differences may affect the amount, timing and character of income distributed to shareholders. The US government and certain foreign

governments have adopted regulations governing derivatives markets, including mandatory clearing of certain derivatives as well as additional regulations governing margin, reporting and registration requirements. The ultimate impact of the

regulations remains unclear. Additional regulation may make derivatives more costly, limit their availability or utility, otherwise adversely affect their performance, or disrupt markets.

(Disclosures and Risks continued on next page)

|

2022 Annual Report |

5 | |

Table of Contents

Disclosures and Risks (continued)

Mortgage-Related

Securities Risk: Mortgage-related securities represent interests in pools of mortgages, including consumer loans or receivables held in trust. Mortgage-related securities are subject to credit, interest-rate, prepayment and extension

risks. These securities also are subject to risk of default on the underlying mortgage, particularly during periods of economic downturn. Small movements in interest rates (both increases and decreases) may quickly and significantly reduce the value

of certain mortgage-related securities. Asset-related securities entail certain risks not presented by mortgage-backed securities, including the risk that it may be difficult to perfect the liens securing any collateral backing certain asset-backed

securities.

Prepayment and Extension Risk: Prepayment risk is the risk that a loan, bond or other security might be called or otherwise

converted, prepaid or redeemed before maturity. If this happens, particularly during a time of declining interest rates or credit spreads, the Portfolio will not benefit from the rise in market price that normally accompanies a decline in interest

rates, and may not be able to invest the proceeds in securities providing as much income, resulting in a lower yield to the Portfolio. Conversely, extension risk is the risk that as interest rates rise or spreads widen, payments of securities may

occur more slowly than anticipated by the market. If this happens, the values of these securities may go down because their interest rates are lower than current market rates and they remain outstanding longer than anticipated.

Subordination Risk: The Portfolio may invest in securities that are subordinated to more senior securities of an issuer, or which represent interests

in pools of such subordinated securities. Subordinated securities will be disproportionately affected by a default or even a perceived decline in creditworthiness of the issuer. Subordinated securities are more likely to suffer a credit loss than non-subordinated securities of the same issuer, any loss incurred by the subordinated securities is likely to be proportionately greater, and any recovery of interest or principal may take more time.

Management Risk: The Portfolio is subject to management risk because it is an actively managed investment portfolio. The Adviser will apply its

investment techniques and risk analyses in making investment decisions for the Portfolio, but these techniques, analyses and decisions may not work as intended or may not produce the desired results, and may, during certain periods, result in

increased volatility for the Portfolio or cause the value of the Portfolios shares to go down. In some cases, derivatives and other investment techniques may be unavailable or the Adviser may determine not to use them, possibly even under

market conditions where their use could benefit the Portfolio. Some of these techniques may incorporate, or rely upon, quantitative models, but there is no guarantee that these models will generate accurate forecasts, reduce risk or otherwise

perform as expected. In addition, the Adviser may change the Portfolios investment strategies or policies from time to time. Those changes may not lead to the results intended by the Adviser and could have an adverse on effect the value or

performance of the Portfolio.

Illiquid Investments Risk: Illiquid investments risk exists when particular investments are difficult or impossible

to purchase or sell, possibly preventing the Portfolio from purchasing or selling these securities at an advantageous price. Over recent years, regulatory changes have led to reduced liquidity in the marketplace, and the capacity of dealers to make

markets in fixed-income securities has been outpaced by the growth in the size of the fixed-income markets. Illiquid investments risk may be magnified in a rising interest-rate environment, where the value and liquidity of fixed-income securities

generally go down.

Redemption Risk: The Portfolio may experience heavy redemptions that could cause the Portfolio to liquidate its assets at

inopportune times or unfavorable prices or increase or accelerate taxable gains or transaction costs and may negatively affect the Portfolios net asset value or performance, which could cause the value of your investment to decline. Redemption

risk is heightened during periods of overall market turmoil.

Foreign Currency Risk: This is the risk that changes in foreign (non-US) currency exchange rates may negatively affect the value of the Portfolios investments or reduce the returns of the Portfolio. For example, the value of the Portfolios investments in foreign

securities and foreign currency positions may decrease if the US dollar is strong (i.e., gaining value relative to other currencies) and other currencies are weak (i.e., losing value relative to the US dollar).

Actions by a Few Major Investors: In certain countries, volatility may be heightened by actions of a few major investors. For example, substantial

increases or decreases in cash flows of mutual funds investing in these markets could significantly affect local securities prices and, therefore, share prices of the Portfolio.

Market Risk: The Portfolio is subject to market risk, which is the risk that stock or bond prices in general or in particular

(Disclosures and Risks continued on next page)

| 6 |

Sanford C. Bernstein Fund II, Inc. |

|

Table of Contents

Disclosures and Risks (continued)

countries or sectors

may decline over short or extended periods. Stock or bond prices may decline in response to adverse changes in the economy or the economic outlook; deterioration in investor sentiment; interest-rate, currency and commodity price fluctuations;

adverse geopolitical, social or environmental developments; issuer- and sector-specific considerations; public health crises (including the occurrence of a contagious disease or illness); policy and legislative changes; cybersecurity events; and

other factors.

Economies and financial markets throughout the world are becoming increasingly interconnected. Economic, financial or political events,

trading and tariff arrangements, sanctions, regional and global conflicts, terrorism, natural disasters (including the spread of infectious illness) and other circumstances in one country or region could have profound impacts on global economies or

markets. As a result, whether or not the Portfolio invests in securities of issuers located in or with significant exposure to countries experiencing economic and financial difficulties, the value and liquidity of the Portfolios investments

may be negatively affected.

Lower-rated Securities Risk: Lower-rated securities, or junk bonds/high-yield securities, are subject to greater risk

of loss of principal and interest and greater market risk than higher-rated securities. The capacity of issuers of lower-rated securities to pay interest and repay principal is more likely to weaken than is that of issuers of higher-rated securities

in times of deteriorating economic conditions or rising interest rates.

These risks are discussed in further detail in the Portfolios prospectus.

An Important Note About Historical Performance

Except as noted, returns do not reflect the deduction of taxes that a shareholder would pay on portfolio distributions or the redemption of portfolio

shares. All fees and expenses related to the operation of the Portfolio have been deducted.

The performance shown in this report represents past

performance and does not guarantee future results. Performance information is as of the dates shown. Current performance may be lower or higher than the performance information shown. You may obtain performance information current to the most recent

month-end by visiting www.Bernstein.com or by calling 212.756.4097. The investment return and principal value of an investment in the Portfolio will fluctuate, so that shares, when redeemed, may be worth more

or less than their original cost.

|

2022 Annual Report |

7 | |

Table of Contents

Historical Performance (Unaudited)

Intermediate Duration Institutional Portfolio vs. Its

Benchmark and Lipper Average

| TOTAL RETURNS | AVERAGE ANNUAL TOTAL RETURNS | |||||||||||||||||||||||

| THROUGH SEPTEMBER 30, 2022 | PAST SIX MONTHS |

PAST 12 MONTHS |

PAST FIVE YEARS |

PAST 10 YEARS |

SINCE INCEPTION |

INCEPTION DATE | ||||||||||||||||||

|

Intermediate Duration Institutional Portfolio1 |

-9.61 | % | -15.13 | % | -0.28 | % | 1.16 | % | 3.55 | % | 5/17/2002 | |||||||||||||

|

Bloomberg US Aggregate Bond Index |

-9.22 | % | -14.60 | % | -0.27 | % | 0.89 | % | 3.35 | % | ||||||||||||||

|

Lipper Core Bond Funds Average |

-9.67 | % | -15.18 | % | -0.34 | % | 0.83 | % | | |||||||||||||||

| 1 | There are no sales charges associated with an investment in the Portfolio. Total returns and average annual returns are therefore the same. |

The current prospectus table shows the total annual operating expense ratio for the Portfolio as 0.52%, gross of any fee waivers or expense reimbursements. Contractual

fee waivers and/or expense reimbursements reduced the total annual operating expense ratio to 0.45%. These waivers/reimbursements may not be terminated before January 28, 2023, and may be extended by the Adviser for additional one-year terms. Absent reimbursements or waivers, performance would have been lower. The Financial Highlights section of this report sets forth expense ratio data for the current reporting period; the expense ratio

shown above may differ from the expense ratio in the Financial Highlights section since they are based on different time periods.

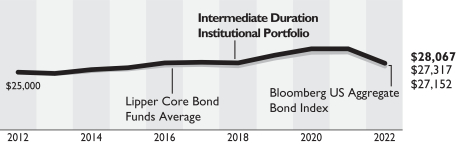

| Growth of a $25,000 Investment in the Portfolio | ||

|

|

The chart illustrates the total value of an assumed $25,000 minimum investment as compared to the performance of the Portfolios

benchmark and Lipper Average for the 10-year period ended September 30, 2022.

Portfolio

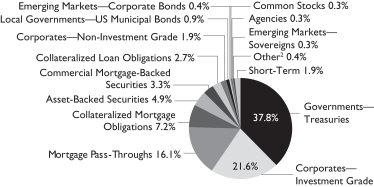

SummarySeptember 30, 2022 (Unaudited)

| Security Type Breakdown1 | ||||

|

||||

| 1 | All data are as of September 30, 2022. The Portfolios security type breakdown is expressed as a percentage of total investments and may vary over time. The Portfolio also enters into derivative transactions, which may be used for hedging or investment purposes (see Schedule of Investments section of the report for additional details). |

| 2 | Other represents less than 0.3% in GovernmentsSovereign Bonds and Quasi-Sovereigns. |

See Disclosures, Risks and Note About Historical Performance on pages 4-7.

| 8 |

Sanford C. Bernstein Fund II, Inc. |

|

Table of Contents

Expense ExampleSeptember 30, 2022 (Unaudited)

As a shareholder of the Fund, you incur various types of costs including management

fees and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an

investment of $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual ExpensesThe first

line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your

account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled Expenses Paid During Period to estimate the expenses you paid on

your account during this period.

Hypothetical Example for Comparison PurposesThe second line of the table below provides information about

hypothetical account values and hypothetical expenses based on the Funds actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Funds actual return. The hypothetical account values and expenses

may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the

5% hypothetical examples that appear in the shareholder reports of other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges

(loads), or contingent deferred sales charges on redemptions. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if

these transactional costs were included, your costs would have been higher.

| BEGINNING ACCOUNT VALUE APRIL 1, 2022 |

ENDING ACCOUNT VALUE SEPTEMBER 30, 2022 |

EXPENSES PAID DURING PERIOD* |

ANNUALIZED EXPENSE RATIO* |

|||||||||||||

|

SCB Intermediate Duration Institutional Portfolio |

||||||||||||||||

|

Actual |

$ | 1,000 | $ | 903.90 | $ | 2.15 | 0.45 | % | ||||||||

|

Hypothetical** |

$ | 1,000 | $ | 1,022.81 | $ | 2.28 | 0.45 | % | ||||||||

| * | Expenses are equal to the classes annualized expense ratios, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). |

| ** | Assumes 5% annual return before expenses. |

|

2022 Annual Report |

9 | |

Table of Contents

Sanford C. Bernstein Fund, Inc.

Schedule of Investments

Intermediate Duration Institutional Portfolio

September 30, 2022

| Principal Amount (000) | U.S. $ Value | |||||||||||

| GOVERNMENTSTREASURIES40.5% |

|

|||||||||||

| United States40.5% |

|

|||||||||||

|

U.S. Treasury Bonds |

U.S.$ | 8,149 | $ | 5,568,990 | ||||||||

|

1.875%, 02/15/2051 |

4,063 | 2,689,330 | ||||||||||

|

2.00%, 11/15/2041 |

6,894 | 4,931,364 | ||||||||||

|

2.00%, 08/15/2051 |

9,349 | 6,383,887 | ||||||||||

|

2.25%, 08/15/2046 |

2,377 | 1,712,854 | ||||||||||

|

2.25%, 08/15/2049 |

15,570 | 11,395,294 | ||||||||||

|

2.25%, 02/15/2052 |

1,672 | 1,214,072 | ||||||||||

|

2.375%, 02/15/2042 |

1,736 | 1,329,939 | ||||||||||

|

2.375%, 11/15/2049 |

4,905 | 3,694,078 | ||||||||||

|

2.50%, 02/15/2046 |

932 | 708,029 | ||||||||||

|

2.50%, 05/15/2046 |

5,327 | 4,040,272 | ||||||||||

|

2.75%, 08/15/2042 |

190 | 154,286 | ||||||||||

|

2.875%, 05/15/2043 |

165 | 135,970 | ||||||||||

|

2.875%, 08/15/2045 |

51 | 41,963 | ||||||||||

|

2.875%, 11/15/2046 |

387 | 316,252 | ||||||||||

|

2.875%, 05/15/2052 |

2,950 | 2,473,768 | ||||||||||

|

3.00%, 05/15/2042 |

843 | 716,945 | ||||||||||

|

3.00%, 11/15/2044 |

200 | 166,843 | ||||||||||

|

3.00%, 05/15/2045 |

129 | 107,298 | ||||||||||

|

3.00%, 11/15/2045 |

363 | 303,242 | ||||||||||

|

3.00%, 05/15/2047(a) |

1,447 | 1,212,315 | ||||||||||

|

3.00%, 02/15/2048 |

5,490 | 4,625,325 | ||||||||||

|

3.125%, 02/15/2043 |

280 | 240,625 | ||||||||||

|

3.125%, 08/15/2044 |

50 | 42,727 | ||||||||||

|

3.25%, 05/15/2042 |

7,885 | 6,995,473 | ||||||||||

|

3.375%, 05/15/2044 |

646 | 575,794 | ||||||||||

|

3.50%, 02/15/2039 |

8,105 | 7,709,881 | ||||||||||

|

3.625%, 08/15/2043 |

1,943 | 1,811,613 | ||||||||||

|

3.625%, 02/15/2044 |

38 | 35,316 | ||||||||||

|

3.75%, 11/15/2043 |

295 | 280,158 | ||||||||||

|

4.375%, 02/15/2038 |

899 | 955,711 | ||||||||||

|

4.375%, 11/15/2039 |

10,740 | 11,327,344 | ||||||||||

|

4.50%, 02/15/2036 |

1,074 | 1,159,872 | ||||||||||

|

4.75%, 02/15/2037 |

1,525 | 1,688,937 | ||||||||||

|

5.375%, 02/15/2031 |

3,646 | 4,024,732 | ||||||||||

|

U.S. Treasury Notes |

67,065 | 65,828,293 | ||||||||||

|

1.375%, 11/15/2031 |

14,097 | 11,449,326 | ||||||||||

|

1.50%, 02/15/2030(b) |

10,851 | 9,209,786 | ||||||||||

|

1.625%, 11/15/2022 |

165 | 164,665 | ||||||||||

|

1.625%, 04/30/2023 |

5,514 | 5,437,321 | ||||||||||

|

1.625%, 05/15/2026 |

43,357 | 39,637,417 | ||||||||||

|

1.625%, 05/15/2031 |

3,253 | 2,730,403 | ||||||||||

|

1.75%, 11/15/2029 |

1,386 | 1,204,087 | ||||||||||

|

2.125%, 12/31/2022 |

11,453 | 11,415,420 | ||||||||||

|

2.625%, 02/15/2029 |

8,921 | 8,221,259 | ||||||||||

|

2.75%, 11/15/2023 |

160 | 157,250 | ||||||||||

|

2.75%, 07/31/2027 |

15,239 | 14,358,090 | ||||||||||

| Principal Amount (000) | U.S. $ Value | |||||||||||

|

2.75%, 08/15/2032 |

U.S.$ | 4,508 | $ | 4,119,707 | ||||||||

|

2.875%, 05/15/2032 |

2,657 | 2,455,557 | ||||||||||

|

3.00%, 07/31/2024 |

20,003 | 19,562,309 | ||||||||||

|

|

|

|||||||||||

| Total GovernmentsTreasuries (cost $325,451,051) |

|

286,721,389 | ||||||||||

|

|

|

|||||||||||

| CORPORATESINVESTMENT GRADE23.2% |

|

|||||||||||

| Industrial12.5% |

|

|||||||||||

| Basic0.8% |

|

|||||||||||

|

Anglo American Capital PLC |

403 | 345,270 | ||||||||||

|

Braskem Netherlands Finance BV |

500 | 401,900 | ||||||||||

|

Celanese US Holdings LLC |

1,494 | 1,473,995 | ||||||||||

|

Freeport Indonesia PT |

324 | 293,220 | ||||||||||

|

Inversiones CMPC SA |

200 | 161,413 | ||||||||||

|

Inversiones CMPC SA/Cayman Islands Branch |

322 | 318,848 | ||||||||||

|

LYB International Finance BV |

187 | 185,201 | ||||||||||

|

LyondellBasell Industries NV |

568 | 572,396 | ||||||||||

|

Suzano Austria GmbH |

343 | 267,540 | ||||||||||

|

WRKCo., Inc. |

1,732 | 1,598,775 | ||||||||||

|

|

|

|||||||||||

| 5,618,558 | ||||||||||||

|

|

|

|||||||||||

| Capital Goods1.0% |

|

|||||||||||

|

CNH Industrial Capital LLC |

1,191 | 1,148,672 | ||||||||||

|

Flowserve Corp. |

1,227 | 878,716 | ||||||||||

|

Parker-Hannifin Corp. |

743 | 655,185 | ||||||||||

|

4.50%, 09/15/2029 |

934 | 884,050 | ||||||||||

|

Raytheon Technologies Corp. |

2,242 | 2,097,839 | ||||||||||

|

Westinghouse Air Brake Technologies Corp. |

270 | 252,296 | ||||||||||

|

4.40%, 03/15/2024 |

1,145 | 1,124,413 | ||||||||||

|

|

|

|||||||||||

| 7,041,171 | ||||||||||||

|

|

|

|||||||||||

| CommunicationsMedia1.3% |

|

|||||||||||

|

Charter Communications Operating LLC/Charter Communications Operating Capital |

467 | 344,599 | ||||||||||

|

Discovery Communications LLC |

509 | 376,467 | ||||||||||

| 10 |

Sanford C. Bernstein Fund II, Inc. |

|

Table of Contents

| Principal Amount (000) | U.S. $ Value | |||||||||||

|

Fox Corp. |

U.S.$ | 700 | $ | 658,070 | ||||||||

|

Interpublic Group of Cos., Inc. (The) |

519 | 480,895 | ||||||||||

|

Prosus NV |

489 | 409,537 | ||||||||||

|

3.68%, 01/21/2030(c) |

639 | 483,787 | ||||||||||

|

4.027%, 08/03/2050(c) |

485 | 272,813 | ||||||||||

|

Tencent Holdings Ltd. |

1,256 | 1,124,355 | ||||||||||

|

3.24%, 06/03/2050(c) |

1,022 | 610,198 | ||||||||||

|

Time Warner Cable LLC |

505 | 350,117 | ||||||||||

|

Warnermedia Holdings, Inc. |

1,826 | 1,503,455 | ||||||||||

|

Weibo Corp. |

3,313 | 2,441,888 | ||||||||||

|

|

|

|||||||||||

| 9,056,181 | ||||||||||||

|

|

|

|||||||||||

| Consumer CyclicalAutomotive0.3% |

|

|||||||||||

|

General Motors Co. |

278 | 278,623 | ||||||||||

|

General Motors Financial Co., Inc. |

171 | 149,001 | ||||||||||

|

Harley-Davidson Financial Services, Inc. |

930 | 797,884 | ||||||||||

|

3.35%, 06/08/2025(c) |

890 | 835,550 | ||||||||||

|

|

|

|||||||||||

| 2,061,058 | ||||||||||||

|

|

|

|||||||||||

| Consumer CyclicalOther0.4% |

|

|||||||||||

|

Las Vegas Sands Corp. |

2,303 | 1,908,473 | ||||||||||

|

MDC Holdings, Inc. |

968 | 737,529 | ||||||||||

|

|

|

|||||||||||

| 2,646,002 | ||||||||||||

|

|

|

|||||||||||

| Consumer CyclicalRetailers0.4% |

|

|||||||||||

|

Lowes Cos., Inc. |

1,126 | 1,035,334 | ||||||||||

|

Ross Stores, Inc. |

1,925 | 1,879,859 | ||||||||||

|

|

|

|||||||||||

| 2,915,193 | ||||||||||||

|

|

|

|||||||||||

| Consumer Non-Cyclical1.1% |

|

|||||||||||

|

Altria Group, Inc. |

1,745 | 1,415,841 | ||||||||||

|

BAT Capital Corp. |

2,706 | 2,155,302 | ||||||||||

|

4.906%, 04/02/2030 |

917 | 807,840 | ||||||||||

|

Cigna Corp. |

740 | 698,834 | ||||||||||

|

CVS Health Corp. |

87 | 82,286 | ||||||||||

|

Ochsner LSU Health System of North Louisiana |

1,480 | 1,131,860 | ||||||||||

| Principal Amount (000) | U.S. $ Value | |||||||||||

|

Takeda Pharmaceutical Co., Ltd. |

U.S.$ | 1,378 | $ | 1,378,000 | ||||||||

|

|

|

|||||||||||

| 7,669,963 | ||||||||||||

|

|

|

|||||||||||

| Energy3.4% |

|

|||||||||||

|

BP Capital Markets America, Inc. |

2,985 | 1,895,326 | ||||||||||

|

Conocophillips Co. |

85 | 68,265 | ||||||||||

|

Continental Resources, Inc./OK |

1,353 | 988,461 | ||||||||||

|

5.75%, 01/15/2031(c) |

1,006 | 909,193 | ||||||||||

|

Devon Energy Corp. |

1,190 | 1,068,180 | ||||||||||

|

Enbridge Energy Partners LP |

1,713 | 1,853,363 | ||||||||||

|

Energy Transfer LP |

100 | 99,540 | ||||||||||

|

6.25%, 04/15/2049 |

882 | 787,811 | ||||||||||

|

EQT Corp. |

451 | 442,891 | ||||||||||

|

Marathon Oil Corp. |

1,800 | 1,800,648 | ||||||||||

|

Marathon Petroleum Corp. |

2,794 | 2,750,162 | ||||||||||

|

6.50%, 03/01/2041 |

415 | 410,916 | ||||||||||

|

MPLX LP |

2,687 | 2,214,222 | ||||||||||

|

Oleoducto Central SA |

491 | 380,003 | ||||||||||

|

ONEOK Partners LP |

73 | 64,798 | ||||||||||

|

ONEOK, Inc. |

1,720 | 1,580,198 | ||||||||||

|

4.35%, 03/15/2029 |

1,012 | 903,382 | ||||||||||

|

6.35%, 01/15/2031 |

263 | 258,061 | ||||||||||

|

Plains All American Pipeline LP/PAA Finance Corp. |

1,059 | 883,407 | ||||||||||

|

4.50%, 12/15/2026 |

683 | 646,364 | ||||||||||

|

Suncor Energy, Inc. |

1,377 | 1,394,268 | ||||||||||

|

Tengizchevroil Finance Co. International Ltd. |

415 | 294,987 | ||||||||||

|

TransCanada PipeLines Ltd. |

1,356 | 1,309,557 | ||||||||||

|

6.20%, 10/15/2037 |

829 | 821,523 | ||||||||||

|

Transcontinental Gas Pipe Line Co., LLC |

449 | 379,185 | ||||||||||

|

|

|

|||||||||||

| 24,204,711 | ||||||||||||

|

|

|

|||||||||||

| Other Industrial0.1% |

|

|||||||||||

|

Alfa SAB de CV |

915 | 907,227 | ||||||||||

|

|

|

|||||||||||

|

2022 Annual Report |

11 | |

Table of Contents

Schedule of Investments (continued)

| Principal Amount (000) | U.S. $ Value | |||||||||||

| Services0.3% |

|

|||||||||||

|

Expedia Group, Inc. |

U.S.$ | 49 | $ | 49,299 | ||||||||

|

Global Payments, Inc. |

275 | 210,724 | ||||||||||

|

3.20%, 08/15/2029 |

845 | 704,874 | ||||||||||

|

5.40%, 08/15/2032 |

944 | 875,145 | ||||||||||

|

S&P Global, Inc. |

411 | 386,459 | ||||||||||

|

4.75%, 08/01/2028(c) |

83 | 81,138 | ||||||||||

|

|

|

|||||||||||

| 2,307,639 | ||||||||||||

|

|

|

|||||||||||

| Technology3.1% |

|

|||||||||||

|

Apple, Inc. |

1,148 | 941,222 | ||||||||||

|

Baidu, Inc. |

203 | 175,079 | ||||||||||

|

Broadcom, Inc. |

323 | 226,465 | ||||||||||

|

3.187%, 11/15/2036(c) |

1,539 | 1,053,800 | ||||||||||

|

4.00%, 04/15/2029(c) |

169 | 148,979 | ||||||||||

|

4.15%, 11/15/2030 |

371 | 320,663 | ||||||||||

|

4.15%, 04/15/2032(c) |

601 | 505,669 | ||||||||||

|

4.926%, 05/15/2037(c) |

1,079 | 892,624 | ||||||||||

|

Entegris Escrow Corp. |

1,270 | 1,126,630 | ||||||||||

|

Fiserv, Inc. |

2,539 | 2,212,485 | ||||||||||

|

HP, Inc. |

1,907 | 1,691,337 | ||||||||||

|

Infor, Inc. |

649 | 584,347 | ||||||||||

|

Intel Corp. |

1,536 | 1,333,371 | ||||||||||

|

International Business Machines Corp. |

1,499 | 1,313,829 | ||||||||||

|

Kyndryl Holdings, Inc. |

2,545 | 2,044,115 | ||||||||||

|

NXP BV/NXP Funding LLC |

1,300 | 1,272,375 | ||||||||||

|

NXP BV/NXP Funding LLC/NXP USA, Inc. |

875 | 732,620 | ||||||||||

|

Oracle Corp. |

1,479 | 1,165,082 | ||||||||||

|

3.60%, 04/01/2040 |

840 | 569,629 | ||||||||||

|

3.65%, 03/25/2041 |

455 | 308,854 | ||||||||||

|

5.375%, 07/15/2040 |

270 | 224,834 | ||||||||||

|

SK Hynix, Inc. |

532 | 391,785 | ||||||||||

|

TSMC Arizona Corp. |

685 | 652,606 | ||||||||||

|

Western Digital Corp. |

1,444 | 985,905 | ||||||||||

|

Workday, Inc. |

242 | 217,040 | ||||||||||

| Principal Amount (000) | U.S. $ Value | |||||||||||

|

3.80%, 04/01/2032 |

U.S.$ | 643 | $ | 559,359 | ||||||||

|

|

|

|||||||||||

| 21,650,704 | ||||||||||||

|

|

|

|||||||||||

| TransportationAirlines0.1% |

|

|||||||||||

|

Delta Air Lines, Inc./SkyMiles IP Ltd. |

819 | 795,740 | ||||||||||

|

|

|

|||||||||||

| TransportationRailroads0.1% |

|

|||||||||||

|

Lima Metro Line 2 Finance Ltd. |

245 | 214,484 | ||||||||||

|

5.875%, 07/05/2034(c) |

398 | 376,536 | ||||||||||

|

|

|

|||||||||||

| 591,020 | ||||||||||||

|

|

|

|||||||||||

| TransportationServices0.1% | ||||||||||||

|

Ashtead Capital, Inc. |

351 | 325,307 | ||||||||||

|

ENA Master Trust |

380 | 279,537 | ||||||||||

|

|

|

|||||||||||

| 604,844 | ||||||||||||

|

|

|

|||||||||||

| 88,070,011 | ||||||||||||

|

|

|

|||||||||||

| Financial Institutions10.3% |

|

|||||||||||

| Banking7.1% |

|

|||||||||||

|

ABN AMRO Bank NV |

269 | 258,399 | ||||||||||

|

Banco de Credito del Peru S.A. |

1,447 | 1,268,657 | ||||||||||

|

Banco Santander SA |

200 | 173,754 | ||||||||||

|

4.175%, 03/24/2028 |

800 | 723,832 | ||||||||||

|

Bank of America Corp. |

924 | 691,401 | ||||||||||

|

2.687%, 04/22/2032 |

2,071 | 1,613,806 | ||||||||||

|

4.376%, 04/27/2028 |

1,652 | 1,548,634 | ||||||||||

|

Bank of Ireland Group PLC |

571 | 558,992 | ||||||||||

|

Barclays PLC |

1,052 | 1,011,182 | ||||||||||

|

BNP Paribas SA |

751 | 642,383 | ||||||||||

|

7.75%, 08/16/2029(c)(d) |

1,517 | 1,405,409 | ||||||||||

|

Capital One Financial Corp. |

1,186 | 994,924 | ||||||||||

|

4.927%, 05/10/2028 |

1,205 | 1,146,991 | ||||||||||

|

Citigroup, Inc. |

941 | 835,392 | ||||||||||

|

4.075%, 04/23/2029 |

1,397 | 1,265,165 | ||||||||||

|

5.95%, 01/30/2023(d) |

481 | 475,483 | ||||||||||

|

Series W |

788 | 664,914 | ||||||||||

|

Series Y |

139 | 111,003 | ||||||||||

|

Credit Suisse Group AG |

1,865 | 1,311,300 | ||||||||||

|

4.194%, 04/01/2031(c) |

799 | 632,337 | ||||||||||

|

6.373%, 07/15/2026(c) |

1,346 | 1,301,084 | ||||||||||

| 12 |

Sanford C. Bernstein Fund II, Inc. |

|

Table of Contents

| Principal Amount (000) | U.S. $ Value | |||||||||||

|

Danske Bank A/S |

U.S.$ | 1,744 | $ | 1,713,829 | ||||||||

|

Deutsche Bank AG/New York NY |

958 | 814,463 | ||||||||||

|

3.961%, 11/26/2025 |

385 | 359,274 | ||||||||||

|

6.119%, 07/14/2026 |

914 | 888,161 | ||||||||||

|

Discover Bank |

386 | 370,799 | ||||||||||

|

Federation des Caisses Desjardins du Quebec |

1,523 | 1,438,671 | ||||||||||

|

Goldman Sachs Group, Inc. (The) |

739 | 558,233 | ||||||||||

|

2.615%, 04/22/2032 |

1,862 | 1,443,478 | ||||||||||

|

Series V |

764 | 607,113 | ||||||||||

|

HSBC Holdings PLC |

715 | 590,254 | ||||||||||

|

5.402%, 08/11/2033 |

581 | 514,342 | ||||||||||

|

6.375%, 03/30/2025(d) |

2,746 | 2,464,810 | ||||||||||

|

JPMorgan Chase & Co. |

2,363 | 1,828,726 | ||||||||||

|

4.851%, 07/25/2028 |

1,570 | 1,506,384 | ||||||||||

|

Series I |

605 | 602,277 | ||||||||||

|

Series V |

27 | 27,000 | ||||||||||

|

Lloyds Banking Group PLC |

250 | 247,167 | ||||||||||

|

Mizuho Financial Group, Inc. |

1,480 | 1,447,100 | ||||||||||

|

Morgan Stanley |

1,502 | 1,353,497 | ||||||||||

|

4.21%, 04/20/2028 |

1,110 | 1,038,250 | ||||||||||

|

Nationwide Building Society |

1,238 | 1,065,769 | ||||||||||

|

Santander Holdings USA, Inc. |

1,584 | 1,522,446 | ||||||||||

|

Santander UK Group Holdings PLC |

1,150 | 1,142,996 | ||||||||||

|

Societe Generale SA |

2,339 | 1,972,409 | ||||||||||

|

Standard Chartered PLC |

885 | 831,847 | ||||||||||

|

4.316% (LIBOR 3 Month + 1.51%), 01/30/2027(c)(d)(e) |

400 | 302,740 | ||||||||||

|

7.75%, 04/02/2023(c)(d) |

200 | 196,002 | ||||||||||

|

Swedbank AB |

600 | 555,114 | ||||||||||

|

UBS Group AG |

256 | 243,195 | ||||||||||

|

7.00%, 02/19/2025(c) |

200 | 189,900 | ||||||||||

|

UniCredit SpA |

459 | 393,101 | ||||||||||

| Principal Amount (000) | U.S. $ Value | |||||||||||

|

US Bancorp |

U.S.$ | 723 | $ | 617,334 | ||||||||

|

Wells Fargo & Co. |

2,052 | 1,667,763 | ||||||||||

|

3.584%, 05/22/2028 |

559 | 505,627 | ||||||||||

|

Series BB |

635 | 537,788 | ||||||||||

|

|

|

|||||||||||

| 50,192,901 | ||||||||||||

|

|

|

|||||||||||

| Brokerage0.4% | ||||||||||||

|

Charles Schwab Corp. (The) |

1,949 | 1,606,873 | ||||||||||

|

Nomura Holdings, Inc. |

1,881 | 1,423,522 | ||||||||||

|

|

|

|||||||||||

| 3,030,395 | ||||||||||||

|

|

|

|||||||||||

| Finance1.3% | ||||||||||||

|

Air Lease Corp. |

702 | 547,195 | ||||||||||

|

2.875%, 01/15/2026 |

175 | 156,898 | ||||||||||

|

3.625%, 04/01/2027 |

76 | 67,330 | ||||||||||

|

Aircastle Ltd. |

2,065 | 1,581,687 | ||||||||||

|

4.125%, 05/01/2024 |

359 | 345,677 | ||||||||||

|

4.25%, 06/15/2026 |

128 | 114,787 | ||||||||||

|

5.25%, 08/11/2025(c) |

906 | 853,443 | ||||||||||

|

Aviation Capital Group LLC |

1,131 | 949,689 | ||||||||||

|

1.95%, 09/20/2026(c) |

390 | 315,873 | ||||||||||

|

3.50%, 11/01/2027(c) |

318 | 264,163 | ||||||||||

|

4.125%, 08/01/2025(c) |

10 | 9,162 | ||||||||||

|

4.375%, 01/30/2024(c) |

312 | 301,579 | ||||||||||

|

4.875%, 10/01/2025(c) |

350 | 326,921 | ||||||||||

|

5.50%, 12/15/2024(c) |

879 | 850,696 | ||||||||||

|

CDBL Funding 1 |

1,460 | 1,333,155 | ||||||||||

|

Synchrony Financial |

1,255 | 891,577 | ||||||||||

|

3.95%, 12/01/2027 |

164 | 142,939 | ||||||||||

|

4.50%, 07/23/2025 |

193 | 184,041 | ||||||||||

|

4.875%, 06/13/2025 |

221 | 213,462 | ||||||||||

|

|

|

|||||||||||

| 9,450,274 | ||||||||||||

|

|

|

|||||||||||

| Insurance0.7% | ||||||||||||

|

Elevance Health, Inc. |

33 | 32,900 | ||||||||||

|

Guardian Life Insurance Co. of America (The) |

868 | 711,456 | ||||||||||

|

Massachusetts Mutual Life Insurance Co. |

11 | 7,340 | ||||||||||

|

MetLife Capital Trust IV |

970 | 1,039,074 | ||||||||||

|

MetLife, Inc. |

25 | 32,614 | ||||||||||

|

2022 Annual Report |

13 | |

Table of Contents

Schedule of Investments (continued)

| Principal Amount (000) | U.S. $ Value | |||||||||||

|

Nationwide Mutual Insurance Co. |

U.S.$ | 377 | $ | 483,680 | ||||||||

|

Prudential Financial, Inc. |

462 | 441,584 | ||||||||||

|

5.375%, 05/15/2045 |

139 | 132,036 | ||||||||||

|

5.625%, 06/15/2043 |

289 | 284,159 | ||||||||||

|

Swiss Re Finance Luxembourg SA |

1,400 | 1,232,504 | ||||||||||

|

Voya Financial, Inc. |

742 | 728,763 | ||||||||||

|

|

|

|||||||||||

| 5,126,110 | ||||||||||||

|

|

|

|||||||||||

| REITs0.8% | ||||||||||||

|

American Tower Corp. |

845 | 774,468 | ||||||||||

|

4.05%, 03/15/2032 |

415 | 357,290 | ||||||||||

|

Digital Realty Trust LP |

1,584 | 1,387,473 | ||||||||||

|

GLP Capital LP/GLP Financing II, Inc. |

1,181 | 886,104 | ||||||||||

|

Host Hotels & Resorts LP |

480 | 352,277 | ||||||||||

|

Vornado Realty LP |

2,003 | 1,530,673 | ||||||||||

|

|

|

|||||||||||

| 5,288,285 | ||||||||||||

|

|

|

|||||||||||

| 73,087,965 | ||||||||||||

|

|

|

|||||||||||

| Utility0.4% |

|

|||||||||||

| Electric0.3% |

|

|||||||||||

|

AES Panama Generation Holdings SRL |

487 | 383,512 | ||||||||||

|

Chile Electricity Pec SpA |

1,040 | 734,500 | ||||||||||

|

Duke Energy Carolinas NC Storm Funding LLC |

920 | 675,216 | ||||||||||

|

Engie Energia Chile SA |

981 | 740,655 | ||||||||||

|

|

|

|||||||||||

| 2,533,883 | ||||||||||||

|

|

|

|||||||||||

| Other Utility0.1% | ||||||||||||

|

American Water Capital Corp. |

438 | 390,000 | ||||||||||

|

|

|

|||||||||||

| 2,923,883 | ||||||||||||

|

|

|

|||||||||||

| Total CorporatesInvestment Grade (cost $196,414,197) |

|

164,081,859 | ||||||||||

|

|

|

|||||||||||

| MORTGAGE PASS-THROUGHS 17.2% |

|

|||||||||||

| Agency Fixed Rate 30-Year16.7% |

|

|||||||||||

|

Federal Home Loan Mortgage Corp. |

492 | 448,362 | ||||||||||

| Principal Amount (000) | U.S. $ Value | |||||||||||

|

3.50%, 11/01/2049 |

U.S.$ | 651 | $ | 592,368 | ||||||||

|

Series 2020 |

1,439 | 1,313,152 | ||||||||||

|

Series 2022 |

6,545 | 5,318,942 | ||||||||||

|

2.50%, 04/01/2052 |

7,637 | 6,435,846 | ||||||||||

|

3.00%, 03/01/2052 |

4,200 | 3,672,742 | ||||||||||

|

Federal Home Loan Mortgage Corp. Gold |

19 | 19,154 | ||||||||||

|

Series 2007 |

147 | 149,823 | ||||||||||

|

Series 2016 |

1,041 | 1,005,774 | ||||||||||

|

Series 2017 |

673 | 648,676 | ||||||||||

|

Series 2018 |

329 | 318,285 | ||||||||||

|

4.50%, 10/01/2048 |

669 | 647,841 | ||||||||||

|

4.50%, 11/01/2048 |

999 | 967,017 | ||||||||||

|

5.00%, 11/01/2048 |

369 | 365,458 | ||||||||||

|

Federal National Mortgage Association |

117 | 119,530 | ||||||||||

|

5.50%, 07/01/2033 |

221 | 225,537 | ||||||||||

|

Series 2004 |

2 | 2,351 | ||||||||||

|

5.50%, 04/01/2034 |

54 | 54,743 | ||||||||||

|

5.50%, 05/01/2034 |

45 | 45,887 | ||||||||||

|

5.50%, 11/01/2034 |

206 | 210,374 | ||||||||||

|

Series 2005 |

322 | 328,641 | ||||||||||

|

Series 2006 |

62 | 63,870 | ||||||||||

|

Series 2007 |

3 | 3,058 | ||||||||||

|

5.50%, 09/01/2036 |

2 | 1,889 | ||||||||||

|

5.50%, 08/01/2037 |

79 | 81,049 | ||||||||||

|

Series 2008 |

0 | ** | 456 | |||||||||

|

Series 2009 |

11 | 11,513 | ||||||||||

|

Series 2010 |

435 | 419,505 | ||||||||||

|

5.00%, 06/01/2040 |

11 | 10,613 | ||||||||||

|

Series 2012 |

376 | 352,959 | ||||||||||

|

3.50%, 11/01/2042 |

3,906 | 3,602,953 | ||||||||||

|

3.50%, 01/01/2043 |

661 | 609,925 | ||||||||||

|

Series 2013 |

2,263 | 2,087,470 | ||||||||||

|

4.00%, 10/01/2043 |

1,484 | 1,405,670 | ||||||||||

|

Series 2015 |

539 | 479,676 | ||||||||||

|

3.00%, 08/01/2045 |

830 | 738,398 | ||||||||||

| 14 |

Sanford C. Bernstein Fund II, Inc. |

|

Table of Contents

| Principal Amount (000) | U.S. $ Value | |||||||||||

|

Series 2018 |

U.S.$ | 1,441 | $ | 1,394,106 | ||||||||

|

Series 2019 |

1,916 | 1,744,994 | ||||||||||

|

3.50%, 09/01/2049 |

682 | 621,671 | ||||||||||

|

3.50%, 11/01/2049 |

1,307 | 1,189,644 | ||||||||||

|

Series 2020 |

1,341 | 1,221,917 | ||||||||||

|

Series 2021 |

6,779 | 5,498,308 | ||||||||||

|

2.50%, 01/01/2052 |

2,154 | 1,817,768 | ||||||||||

|

Series 2022 |

4,715 | 3,970,415 | ||||||||||

|

2.50%, 04/01/2052 |

5,001 | 4,211,488 | ||||||||||

|

2.50%, 05/01/2052 |

6,370 | 5,364,484 | ||||||||||

|

3.00%, 02/01/2052 |

5,145 | 4,500,178 | ||||||||||

|

3.00%, 03/01/2052 |

6,535 | 5,714,324 | ||||||||||

|

Government National Mortgage Association |

179 | 160,672 | ||||||||||

|

3.00%, 05/20/2046 |

518 | 465,282 | ||||||||||

|

Series 2022 |

1,480 | 1,306,541 | ||||||||||

|

4.00%, 10/01/2052, TBA |

3,275 | 3,055,173 | ||||||||||

|

4.50%, 10/01/2052, TBA |

7,442 | 7,114,132 | ||||||||||

|

Uniform Mortgage-Backed Security |

13,171 | 10,657,398 | ||||||||||

|

2.50%, 10/01/2052, TBA |

18,727 | 15,714,586 | ||||||||||

|

3.00%, 10/01/2052, TBA |

5,384 | 4,680,934 | ||||||||||

|

4.00%, 10/01/2052, TBA |

5,776 | 5,353,393 | ||||||||||

|

|

|

|||||||||||

| 118,516,915 | ||||||||||||

|

|

|

|||||||||||

| Agency Fixed Rate 15-Year0.5% |

|

|||||||||||

|

Federal National Mortgage Association |

48 | 44,049 | ||||||||||

|

2.50%, 11/01/2031 |

2,631 | 2,411,923 | ||||||||||

|

2.50%, 12/01/2031 |

13 | 11,576 | ||||||||||

|

Series 2017 |

709 | 649,376 | ||||||||||

|

2.50%, 02/01/2032 |

631 | 577,573 | ||||||||||

|

|

|

|||||||||||

| 3,694,497 | ||||||||||||

|

|

|

|||||||||||

| Other Agency Fixed Rate Programs0.0% |

|

|||||||||||

|

Federal National Mortgage Association |

20 | 20,018 | ||||||||||

|

|

|

|||||||||||

| Agency ARMs0.0% |

|

|||||||||||

|

Federal Home Loan Mortgage Corp. Gold |

0 | ** | 125 | |||||||||

|

Series 2007 |

0 | ** | 370 | |||||||||

| Principal Amount (000) | U.S. $ Value | |||||||||||

|

Federal National Mortgage Association |

U.S.$ | 1 | $ | 1,006 | ||||||||

|

2.52% (LIBOR 12 Month + 1.80%), 03/01/2037(e) |

0 | ** | 456 | |||||||||

|

|

|

|||||||||||

| 1,957 | ||||||||||||

|

|

|

|||||||||||

| Total Mortgage Pass-Throughs (cost $132,994,550) |

|

122,233,387 | ||||||||||

|

|

|

|||||||||||

| COLLATERALIZED MORTGAGE OBLIGATIONS7.7% |

|

|||||||||||

| Risk Share Floating Rate6.6% |

|

|||||||||||

|

Bellemeade Re Ltd. |

226 | 225,775 | ||||||||||

|

Series 2019-3A, Class M1B |

227 | 227,010 | ||||||||||

|

Series 2019-3A, Class M1C |

300 | 296,394 | ||||||||||

|

Series 2020-3A, Class M1B |

88 | 88,164 | ||||||||||

|

Series 2021-1A, Class M1C |

1,036 | 1,002,192 | ||||||||||

|

Series 2021-2A, Class M1B |

1,892 | 1,828,527 | ||||||||||

|

Series 2021-3A, Class A2 |

1,894 | 1,780,284 | ||||||||||

|

Series 2022-1, Class M1B |

1,000 | 977,873 | ||||||||||

|

Connecticut Avenue Securities Trust |

1,550 | 1,548,233 | ||||||||||

|

Series 2022-R07, Class 1M1 |

2,096 | 2,095,698 | ||||||||||

|

Connecticut Avenue Securities Trust |

2,037 | 1,991,603 | ||||||||||

|

Series 2022-R01, Class 1M2 |

2,306 | 2,099,693 | ||||||||||

|

Series 2022-R02, Class 2M1 |

1,913 | 1,873,130 | ||||||||||

|

2022 Annual Report |

15 | |

Table of Contents

Schedule of Investments (continued)

| Principal Amount (000) | U.S. $ Value | |||||||||||

|

Series 2022-R03, Class 1M2 |

U.S.$ | 1,545 | $ | 1,467,295 | ||||||||

|

Series 2022-R05, Class 2M2 |

1,206 | 1,112,946 | ||||||||||

|

Eagle Re Ltd. |

217 | 215,466 | ||||||||||

|

Series 2020-1, Class M1A |

17 | 17,426 | ||||||||||

|

Series 2021-2, Class M1B |

650 | 631,957 | ||||||||||

|

Federal Home Loan Mortgage Corp. |

1,358 | 1,289,921 | ||||||||||

|

Federal Home Loan Mortgage Corp. |

315 | 318,124 | ||||||||||

|

Series 2020-DNA5, Class M2 |

655 | 655,367 | ||||||||||

|

Series 2021-DNA3, Class M2 |

779 | 741,627 | ||||||||||

|

Series 2021-DNA5, Class M2 |

652 | 636,217 | ||||||||||

|

Series 2021-DNA6, Class M2 |

2,513 | 2,280,811 | ||||||||||

|

Series 2021-DNA7, Class M2 |

2,412 | 2,161,331 | ||||||||||

|

Series 2021-HQA4, Class M2 |

1,530 | 1,300,513 | ||||||||||

|

Series 2022-DNA1, Class M1A |

952 | 924,270 | ||||||||||

|

Series 2022-DNA1, Class M1B |

1,223 | 1,110,088 | ||||||||||

|

Series 2022-DNA2, Class M1B |

1,717 | 1,594,535 | ||||||||||

|

Series 2022-DNA3, Class M1B |

711 | 671,287 | ||||||||||

| Principal Amount (000) | U.S. $ Value | |||||||||||

|

Series 2022-DNA5, Class M1B |

U.S.$ | 2,274 | $ | 2,278,701 | ||||||||

|

Series 2022-DNA6, Class M1A |

803 | 798,280 | ||||||||||

|

Series 2022-DNA7, Class M1A |

2,142 | 2,142,998 | ||||||||||

|

Series 2022-HQA1, Class M1B |

399 | 381,778 | ||||||||||

|

Federal National Mortgage Association Connecticut Avenue Securities |

123 | 126,982 | ||||||||||

|

Series 2021-R02, Class 2M2 |

1,071 | 957,119 | ||||||||||

|

Home Re Ltd. |

1,162 | 1,136,169 | ||||||||||

|

JPMorgan Madison Avenue Securities Trust |

47 | 45,203 | ||||||||||

|

Oaktown Re VII Ltd. |

1,767 | 1,734,777 | ||||||||||

|

PMT Credit Risk Transfer Trust |

||||||||||||

|

5.863% (LIBOR 1 Month + 2.75%), 05/27/2023(c)(e) |

749 | 718,827 | ||||||||||

|

Series 2019-3R, Class A |

63 | 60,637 | ||||||||||

|

Series 2020-1R, Class A |

245 | 232,759 | ||||||||||

|

Radnor Re Ltd. |

909 | 897,949 | ||||||||||

|

Series 2019-2, Class M1B |

230 | 229,221 | ||||||||||

|

Series 2020-1, Class M1A |

270 | 268,877 | ||||||||||

|

Traingle Re Ltd. |

1,225 | 1,215,981 | ||||||||||

| 16 |

Sanford C. Bernstein Fund II, Inc. |

|

Table of Contents

| Principal Amount (000) | U.S. $ Value | |||||||||||

|

Wells Fargo Credit Risk Transfer Securities Trust |

U.S.$ | 187 | $ | 172,259 | ||||||||

|

Series 2015-WF1, Class 2M2 |

48 | 44,698 | ||||||||||

|

|

|

|||||||||||

| 46,606,972 | ||||||||||||

|

|

|

|||||||||||

| Agency Fixed Rate0.6% |

|

|||||||||||

|

Federal Home Loan Mortgage Corp. REMICs |

5,454 | 1,108,447 | ||||||||||

|

Series 5015, Class BI |

3,260 | 618,417 | ||||||||||

|

Series 5034, Class BI |

4,400 | 969,783 | ||||||||||

|

Federal National Mortgage Association Grantor Trust |

291 | 261,614 | ||||||||||

|

Federal National Mortgage Association REMICs |

7,042 | 1,331,400 | ||||||||||

|

|

|

|||||||||||

| 4,289,661 | ||||||||||||

|

|

|

|||||||||||

| Agency Floating Rate0.3% |

|

|||||||||||

|

Federal Home Loan Mortgage Corp. REMICs |

1,387 | 131,884 | ||||||||||

|

Series 4693, Class SL |

1,513 | 163,856 | ||||||||||

|

Series 4954, Class SL |

2,144 | 214,517 | ||||||||||

|

Series 4981, Class HS |

4,662 | 458,827 | ||||||||||

|

Federal National Mortgage Association REMICs |

814 | 95,005 | ||||||||||

|

Series 2016-106, Class ES |

1,390 | 142,281 | ||||||||||

|

Series 2017-73, Class SA |

1,787 | 209,237 | ||||||||||

|

Series 2017-97, Class LS |

1,426 | 157,158 | ||||||||||

| Principal Amount (000) | U.S. $ Value | |||||||||||

|

Series 2017-97, Class SW |

U.S.$ | 1,286 | $ | 136,283 | ||||||||

|

Government National Mortgage Association |

1,799 | 194,802 | ||||||||||

|

Series 2017-65, Class ST |

1,605 | 181,083 | ||||||||||

|

Series 2017-134, Class SE |

893 | 84,828 | ||||||||||

|

|

|

|||||||||||

| 2,169,761 | ||||||||||||

|

|

|

|||||||||||

| Non-Agency Floating Rate0.1% |

|

|||||||||||

|

Deutsche Alt-A Securities Mortgage Loan Trust |

863 | 319,872 | ||||||||||

|

HomeBanc Mortgage Trust |

154 | 129,816 | ||||||||||

|

JPMorgan Chase Bank, NA |

198 | 193,447 | ||||||||||

|

|

|

|||||||||||

| 643,135 | ||||||||||||

|

|

|

|||||||||||

| Non-Agency Fixed Rate0.1% |

|

|||||||||||

|

Alternative Loan Trust |

64 | 46,030 | ||||||||||

|

Series 2006-24CB, Class A16 |

379 | 218,877 | ||||||||||

|

Series 2006-28CB, Class A14 |

290 | 164,907 | ||||||||||

|

Series 2006-J1, Class 1A13 |

168 | 121,962 | ||||||||||

|

CHL Mortgage Pass-Through Trust |

74 | 35,213 | ||||||||||

|

|

|

|||||||||||

| 586,989 | ||||||||||||

|

|

|

|||||||||||

| Total Collateralized Mortgage Obligations (cost $56,788,872) |

|

54,296,518 | ||||||||||

|

|

|

|||||||||||

| ASSET-BACKED SECURITIES5.2% |

|

|||||||||||

| Other ABSFixed Rate2.7% |

|

|||||||||||

|

AB Issuer LLC |

2,090 | 1,714,489 | ||||||||||

|

Affirm Asset Securitization Trust |

427 | 414,290 | ||||||||||

|

2022 Annual Report |

17 | |

Table of Contents

Schedule of Investments (continued)

| Principal Amount (000) | U.S. $ Value | |||||||||||

|

Series 2021-Z2, Class A |

U.S.$ | 450 | $ | 433,812 | ||||||||

|

Series 2022-X1, Class A |

1,168 | 1,138,828 | ||||||||||

|

Atalaya Equipment Leasing Trust |

509 | 474,682 | ||||||||||

|

BHG Securitization Trust |

267 | 249,801 | ||||||||||

|

Cajun Global LLC |

440 | 374,068 | ||||||||||

|

College Ave Student Loans LLC |

637 | 539,331 | ||||||||||

|

Conns Receivables Funding LLC |

507 | 504,304 | ||||||||||

|

Dext ABS LLC |

186 | 168,830 | ||||||||||

|

Diamond Infrastructure Funding LLC |

935 | 761,904 | ||||||||||

|

Diamond Issuer |

1,941 | 1,639,607 | ||||||||||

|

Dominos Pizza Master Issuer LLC |

1,055 | 868,487 | ||||||||||

|

FREED ABS Trust |

1,760 | 1,696,120 | ||||||||||

|

GCI Funding I LLC |

658 | 561,473 | ||||||||||

|

Hardees Funding LLC |

716,083 | |||||||||||

|

Series 2020-1A, Class A2 |

481 | 412,890 | ||||||||||

|

MVW LLC |

881 | 785,410 | ||||||||||

|

Neighborly Issuer |

2,003 | 1,611,333 | ||||||||||

|

Neighborly Issuer LLC |

769 | 635,816 | ||||||||||

|

Nelnet Student Loan Trust |

620 | 493,140 | ||||||||||

|

Series 2021-CA, Class B |

907 | 707,037 | ||||||||||

|

Series 2021-DA, Class B |

798 | 643,202 | ||||||||||

| Principal Amount (000) | U.S. $ Value | |||||||||||

|