Recommended by James Stanley

Get Your Free Top Trading Opportunities Forecast

I don’t think that the bear market is over in stocks yet. And it’s worth noting, I’m not a perma-bear, or at least I don’t consider myself one. But, I have been bearish on equities for much of the past year, even setting this as my Top Trade for the second through fourth quarters, and in Q1 I was looking at a related theme of USD-strength.

For next year I think the bearish overhang remains. The Fed may have already gotten in the bulk of the hikes that they’re going to do, but inflation still remains problematic and this will force them to keep rates elevated until either something breaks or inflation begins to give way. And if inflation is going to give way quickly, it’s difficult to imagine a scenario in which that’s happening that doesn’t include some aggressive recessionary factors so, in either scenario it really appears that some pain is on the way before we get some noticeable pivot from the FOMC.

Perhaps more importantly for equities is the transmission impact of rate hikes. Hikes take time to price through an economy and the pace with which rates were hiked last year means that it’s pretty indecipherable how impactful it’s been just yet. But, for corporate earnings, logically, there’s still some impact to be seen. And if rates do remain elevated through the first-half of next year, it’s difficult to imagine corporate earnings not getting hit harder.

And unlike prior instances of economic weakness, the Fed doesn’t have that supportive option of quickly shifting towards looser policy as inflation remains well above-target. And to be sure, this wasn’t an option in 2022 either, but that didn’t stop market participants from pricing in a possible inflation top in June and then a possible Fed pivot in October.

But, inflation didn’t top in June – nor did the Fed say anything that would denote a pivot into dovishness in October. And I think that these are themes that will be dealt with in 2023 trade.

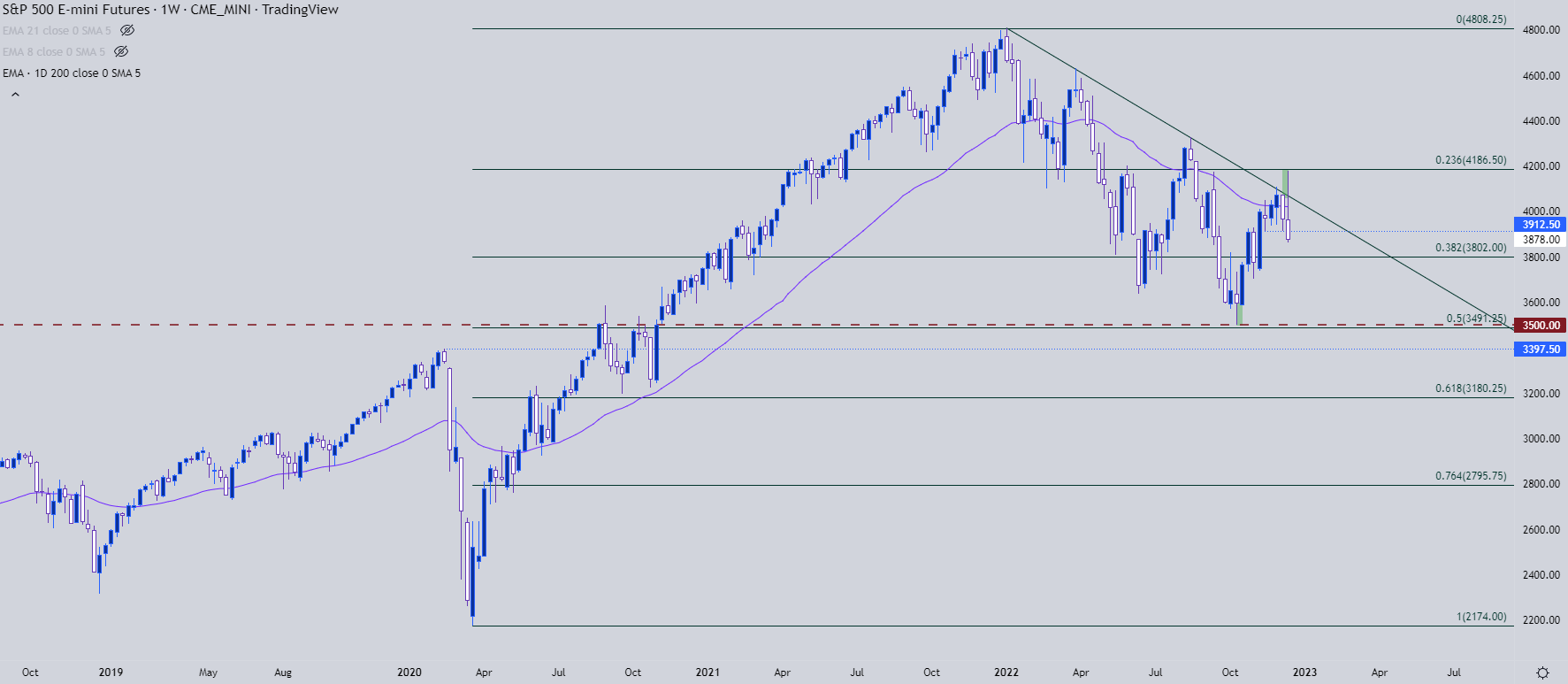

S&P 500

My first support target for the S&P 500 is the 3500 level that currently sits about 9.5% from current prices. This was a level that almost came into play in October with that low printing at 3502. If bears do get to run, there’s another major level around 3200 but that’s now about 17.5% away from current price, which may be a bit aggressive to look for in a single quarter, although it’s possible if we end up in the ‘something breaking’ scenario mentioned above. More likely, the pre-pandemic swing high will create some motivation for support and that plots right around the 3400 level.

S&P 500 Weekly Price Chart

Chart prepared by James Stanley; S&P 500 on Tradingview

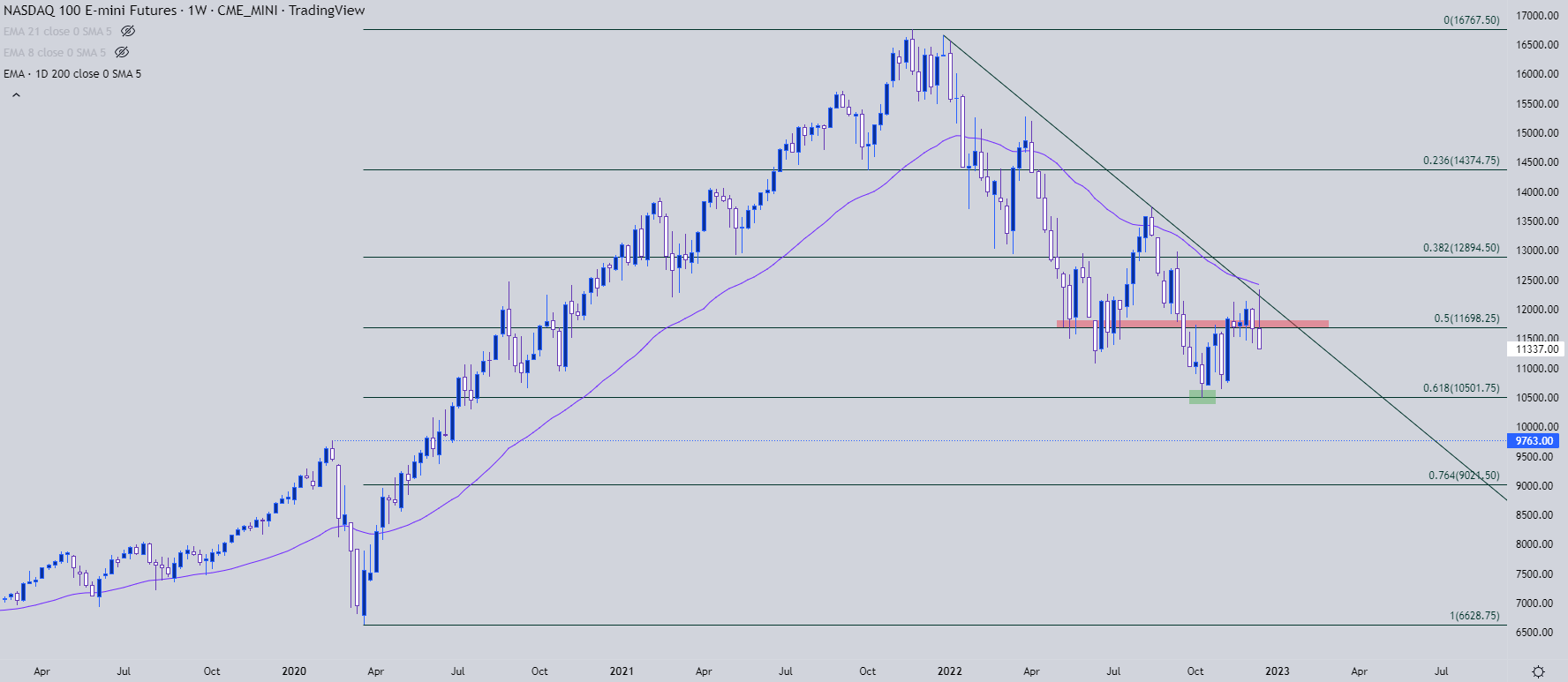

Nasdaq

I’m also bearish the Nasdaq, perhaps even more so than the S&P 500 above. There has been greater development of the bearish theme, as well, with a similarly placed Fibonacci retracement, spanning from the pandemic low to the pandemic high. While the S&P 500 bounced above the 50% mark of its own major move, the Nasdaq set its 2022 low (at least as of this writing) at the 61.8% retracement.

That plots at 10,501 which remains as an initial target. Below that, the 10k psychological level is followed by the pre-pandemic swing-high at 9763, after which the 76.4% Fibonacci retracement shows up just above the 9k handle.

Recommended by James Stanley

Get Your Free Equities Forecast

Nasdaq 100 Weekly Chart

Chart prepared by James Stanley; Nasdaq 100 on Tradingview

GBP/JPY

I wanted to get an FX pair in this installment of Top Trades. I think GBP/JPY could be situated for a fall. While the Bank of Japan has kept policy pedal-to-the-floor, I’m not sure that market rates are in a position where they can rise substantially from here. As recessionary factors stack-up, this could lead to deeper curve inversion as investors buy longer-dated treasuries in anticipation of lower rates at some point down-the-road.

If we do see lower rates in US Treasuries, that’s less motive to use the Yen as a funding source for carry trades, which can lead to further unwind of Yen-weakness. And in regards to the British Pound, the currency feels well-priced at the moment, particularly for an economy with some recessionary factors already flaring.

From a technical standpoint, GBP/JPY hasn’t been able to mount much for recovery above the 170 psychological level yet, and that level can help to keep bearish swing potential in the equation. I’m looking for downside targets at 159.45 and then 148.87, based entirely off of prior price action swings.

GBP/JPY Monthly Price Chart

Chart prepared by James Stanley; Nasdaq 100 on Tradingview

{kind=link}