Across Europe, the emergence of neobanks has been one of the landmark disruptions to financial services over the past eight years.

But despite the hype, these financial disruptors have enjoyed only mixed success and those neobanks which are winning out now face the conundrum of profiting from their increasingly enlarged businesses.

The likes of Revolut, Monzo, Starling, N26 and Bunq have garnered tens of millions of mainly younger customers across the continent, enticed by their whizzy technology, flashy cards and almost cult-like status.

But the quintet, generally speaking, are rare successes in a nearly 300-strong neobank market overwhelmingly populated by loss-making startups, and many which have failed altogether.

Adam Davis, associate partner, Bain Capital, says: “There are so many neobanks and many haven’t made the grade.

“The key principles of those which have been successful have been fantastic user experience, being first to market and attacking a niche.”

But how does one gauge a neobank’s success? Is it by revenues? Brand appeal? Customer numbers? Market Share?

Tech.eu spoke to a bunch of analysts and the consensus was that the trio of metrics: profitability, customer numbers and impact on the banking landscape are as good as any metrics as an indicator of success.

Neobanks hitting the profitability mark

After years of sacrificing profitability at the altar of growth, neobanks are now focusing on profitability, amid restless VC demands for positive numbers.

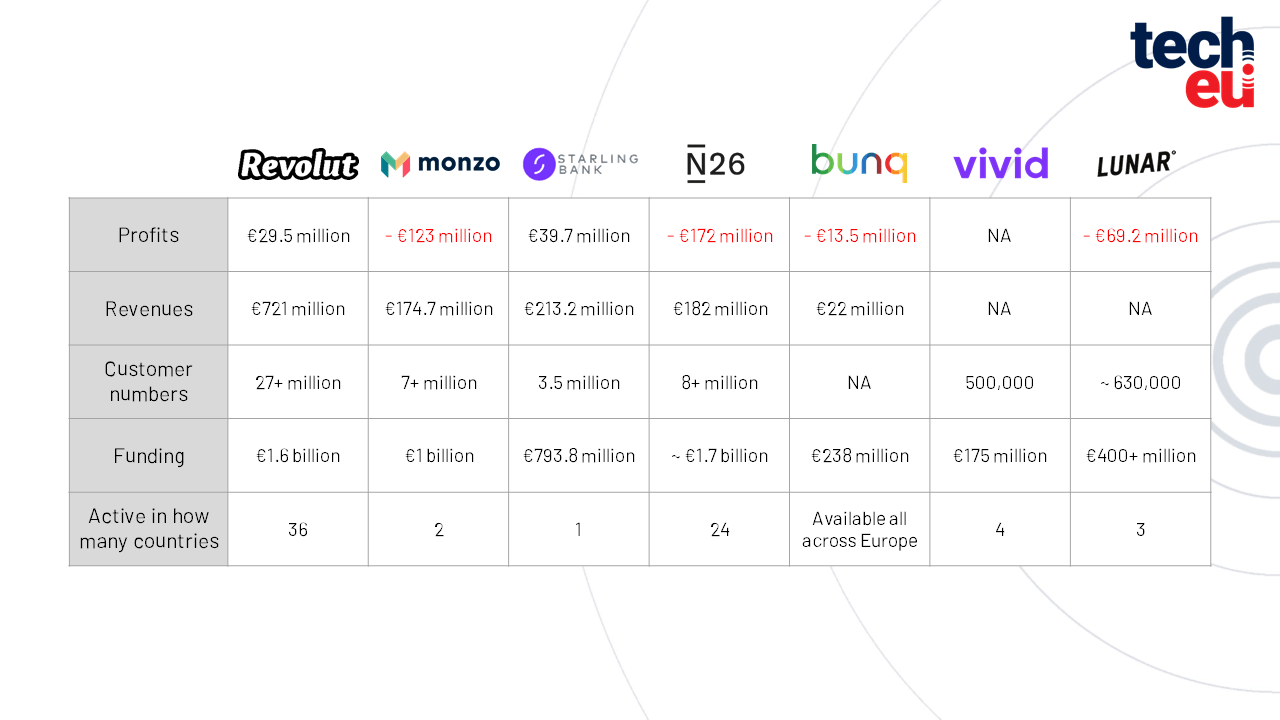

In the UK, Starling, valued at more than £2.5bn, and Revolut, valued at £28bn, have made their first annual profits: Starling £32m in 2022 and Revolut £26m in 2021.

Monzo, valued at £3.8bn, which made a £119m loss in 2022, has said it’s “on track for profitability” by the end of the current financial year.

Though not exactly comparing apples with apples, it is worth pointing out that UK banking giant HSBC made a whopping profit of £14bn in 2022.

Across Europe, Amsterdam-based Bung, valued at £1.6bn, reached quarterly profitability for the last quarter of 2022 and says it expects to continue to turn a profit throughout 2023.

Berlin-based N26, valued at £7.6bn, registered losses in 2021 of £153m while its smaller country rival Vivid Money is on track to be “operationally” profitable by the end of this year.

Meanwhile, Danish neobank Lunar, valued at over £1bn, made a £432,000 loss in 2021 but says profitability is firmly on its radar.

Customer number surging

While not taking a wreaking ball to incumbent banks, the disruptors have undoubtedly dented traditional banks’ customer numbers.

Leading the pack is Revolut which now has a humongous 27m customers (including 2m new customers in the last four months) across 36 markets.

Monzo has over 7m UK customers (including 200,000 potentially lucrative business customers) and is now ranked in the top ten biggest banks in the UK by customer numbers.

Starling has 3.5m customers (including 520,000 SME customers).

Bunq does not disclose customer numbers; Lunar has 630,000 customers and Vivid Money has around 500,000 customers.

Allied to customer numbers, another potential indicator of success could be app download figures.

According to figures from data firm Apptopia (which surveyed European monthly downloads across Revolut, Monzo, Starling, N26, Bunq, Monese), Revolut is in the lead with 64.74 per cent of downloads, ahead of second-placed Monzo (17.19 per cent).

Impact on customer relationship “total”

Davis says a key indicator of neobanks success is the transformational change they’ve engendered in how customers interact with banks, displacing bank branches with seamless, zippy instant online services.

Davis says this is important as it’s the “ticket dined out on when they started”.

Furthermore, the rise of neobanks has undoubtedly ruffled the feathers of established banks.

Kieran Hines, analyst at Celent, says: “The emergence of Monzo, Revolut and others has undoubtedly helped stimulate a lot of investment on the part of big banks who want to catch up and close that gap.”

In the UK market, for example, banking giants HSBC, RBS and NatWest and US giant JP Morgan (which also plans to launch a digital bank in Germany as early as 2024) have launched neobank offshoots to counter the neobank surge.

Neobanks diversifying

Since their inception around eight years ago, neobanks have garnered hundreds of millions of pounds in funding, helping them become some of the most valuable fintechs across Europe.

But many in their early stages have been heavily reliant on card transaction fees as a primary revenue stream, a strategy which is unsustainable in the long-term and precarious amid an economic downturn given its reliance on customer spending.

Cognisant of this, over the past few years, neobanks have been broadening their businesses launching new revenue streams.

Revolut, which began life in 2015 offering cheap foreign exchange fees, has ambitions to be a “super-app” and now has its fingers in multiple pies, including banking services, currency exchange, stock trading, crypto, peer-to-peer payments, travel, insurance and even instant messaging.

Its push into crypto appears to be bearing dividends, with its latest financial figures for its foreign exchange and wealth division (which includes crypto) making up over half (55 per cent) of total revenues in 2021.

Starling has made a big push into SME banking and now holds 8.9 per cent of the UK market share for SME banking, as well as shifting its business into mortgage lending.

Monzo, meanwhile, has vaulted its business into subscriptions, launching Premium and Plus offerings, with subscription revenues jumping to over £11m by last year from launch in 2021.

N26, which is in 24 countries, now spans subscriptions, insurance, crypto and other banking products; likewise, Vivid Money says premium subscriptions are a “major revenue” driver.

Bunq, which bills itself as a sustainable bank, offers banking services, lending products and a real-time budgeting initiative.Lunar, which has a presence in Sweden, Norway and Denmark and counts Hollywood star Will Ferrell as a brand ambassador, is eyeing up a push into mainland Europe.

Lending could be future direction

Which of these strategies will prove the winner will be proven over time, but experts believe lending will be a hot area for neobanks in the future.

“What it comes down to and I think what will be the next phase for what generates profits for these neobanks is lending,” says Rudy Yang, fintech analyst, PitchBook.

But lending is a difficult nut to crack, requiring a large and diversified balance sheet, building credit models and data-driven pricing.

To combat this, in the US, neobanks have partnered with chartered banks (which do the heavy lifting) to offer lending products.

Revolut, which does not yet have a UK banking licence, would have to follow a similar path should it want to become a significant lender in the UK.

But lending can be a perilous strategy, adds Yang, pointing to a risk of delinquencies in the current difficult economic climate.

Hines says credit is where the big money is made in banking but capturing customer deposits to lend out can impact profitability.

“It is easy to lend people money, it is hard to lend money profitability,” adds Hines.

SMBs

Neobanks are increasingly eyeing up the SMB market, an underserved market as a revenue diversifier.

Starling and Lunar are examples of neobanks pursuing this strategy.

“Everyone is comfortable paying fees for business banking services in a way they are much less comfortable in consumer banking so it’s a natural development point to start looking at the audience,” says Hines.

Neobanks, generally speaking, build their business propositions on top of business transaction accounts by then offering the likes of business savings accounts, invoice financing and lending.

Subscriptions

A further way neobanks to increase revenues has been upselling through paid-for subscription offerings, which add reliable monthly recurring revenues to the bottom line.

Revolut said its subscriptions revenues grew from £71m to £107m between 2021 and 2022 while Monzo offers Monzo Premium, which offers phone and travel insurance and other benefits for £15 a month, and a cheaper Monzo Prime, with a holographic card, for £5 a month.

One extra benefit of subscription services, says Bain, is they can bring together an ecosystem of partners outside of financial services, such as loyalty card partners.

The future

In a report on the future of banking, McKinsey said the biggest threat to the banking industry comes from cross-industry firms like Amazon, Google and PayPal, with their ”vastly superior economic” models.

And that in the future increasingly neobanks and traditional banks will have to compete in “new arenas”, organised around customer needs.

But experts are undecided as to whether we will see neobanks competing with tech giants and offer a range of non-financial services in the future.

Hines says the neobanks are already shifting in this direction, pointing to them supporting the integration into accounting platforms but says the shift to non-financial services will not be a ”flick of a switch” moment.

However, shifting outside of their core domain might not be easy, as the some of the tech giants have discovered with their troubled payment offerings.

But Davis says the wind is blowing in the other direction, with the rise of non-financial brands offering financial services through embedded financing.

Which strategy will win out?

Which neobank strategy- be it super-app, SMB-focus, or world domination- will prove the most successful will play out over time.

But it is noticeable that successful neobanks, unlike some of their fintech peers, have largely ridden out the economic downturn and not suffered the ignominy of downrounds and swathes of job cuts.

Experts agree we may see less neobanks in the future, but the successful ones will continue to flourish.

Yang says: “I think the ultimate end goal is you will have multiple revenue streams, you will have multiple products and services from neobanks. And the ones that really stand out will be profitable at the end of the day.”

Also read:

Fintech’s growth potential in a bear market

Empowering a green & sustainable economy – ESG Fintech report

{kind=link}