energyy

Thesis

VEON Ltd. (NASDAQ:VEON) is trading well below its intrinsic value, and multiple possible catalysts exist to unlock the discount.

Overview

VEON is a telecom company operating in Russia, Ukraine, Pakistan, Bangladesh, Kazakhstan, and other ex-Soviet countries. The Telecom industry is capital-intensive, and there are no moats. As long as there is no difference in network quality, people often buy the cheapest plan, which leads to never-ending price wars between operators. Once the expensive capex cycle is finished, there will always be the next G network technology, and the capex starts all over again. As a result, telecoms typically have high debt levels and low returns on invested capital. In the past decade telecom sector underperformed the rest of the stock market.

VEON also used high leverage, mainly borrowing in USD while earning revenues in local currencies. Unfortunately, the operating countries’ currencies depreciated against USD while debt levels stayed the same, so the outcome wasn’t good for VEON. In recent years, VEON has been divesting operations in some countries and selling some of its tower assets to bring down debt levels steadily.

Before the Russian invasion, VEON made around $8 billion in revenues and $500-$1,000 million in free cash flows annually. They also paid out $500 million in annual dividends. Compare that to the current market cap of $1.2 billion.

Balance sheet

The equity is only $776 million. However, in 1H 2022 financial statements, the foreign currency translation reserve was $9 billion negative, which indicates that the assets owned might be more valuable than shown on the balance sheet. The operating companies’ assets are accounted in local currencies, but the consolidated earnings are translated into USD, so when the operating countries’ currencies depreciate against USD, the assets’ accounting balances also fall. Generally, in high inflationary countries, the currency exchange losses are compensated by higher growth rates, although in recent years, the foreign exchange losses surpassed local revenue growth rates. When adding the foreign translation reserve and deducting goodwill, the equity value is around $8 billion.

There is $3.1 billion cash on the balance sheet, of which $2.5 billion is on the HQ level. Gross debt is $6.7 billion leading to net debt of $3.7 billion (excluding leases).

Russian operations sale

Since the Russian invasion, VEON lost its credit rating, making it impossible to refinance maturing debt notes. That’s why they announced selling the Russian operating company for 130 billion rubles, equal to $1.7 billion in today’s exchange rates. After the sale, VEON’s net debt would be around $2 billion. So far, they have received Russian regulatory approval for the sale, and if everything goes as planned, it will be completed by June.

From a pure valuation perspective, the Russian operations divestment will destroy some shareholder value. However, they were forced to do it in order to refinance debt maturities. Once the sale is completed, future political risks will be reduced, and VEON should gain access to the debt refinancing markets again. Therefore, considering the current situation, the sale price was still fair.

VEON also owns $800 million worth of tower assets in other operating countries, which they plan to sell over the next two years. That would bring the net debt levels closer to $1 billion.

Valuation

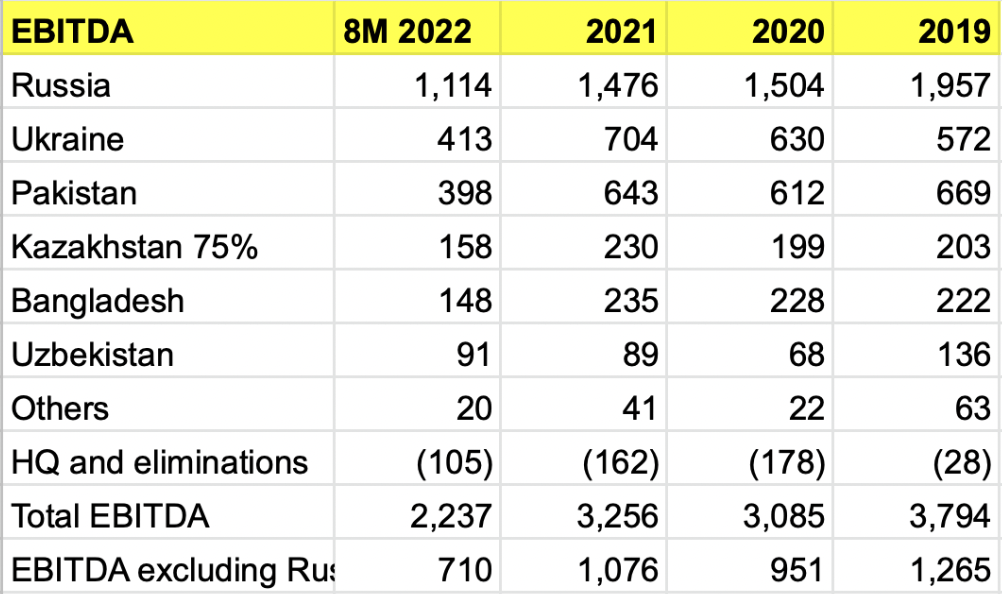

When excluding Russia and Ukraine, they made about $1 billion in EBITDA. Somehow, they are still operating profitably in Ukraine even during the war, but as we don’t know what will happen there, I will exclude Ukraine from the valuation model.

Author’s spreadsheet, sourced from annual reports and market updates

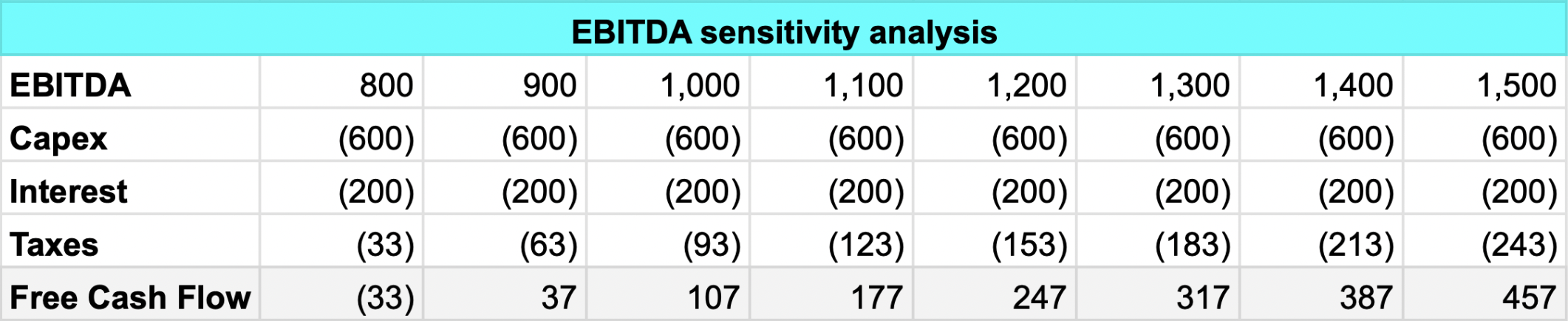

Revenues without Russia and Ukraine are about $3 billion, so with a targeted 20% capex intensity, that is $600 million spent in capex annually.

Let’s say the interest rate on $2 billion net debt will be 10%, leading to a $200 million interest expense. Around $1.2 billion of that debt is on the parent company’s balance sheet, so only about 40% of the interest expense is deductible from taxes.

The average tax rate is around 30% resulting in a $123 million tax expense.

Leading to $107 million in free cash flows.

In 2019 these countries made $1,265 EBITDA, which would result in just under $300 million in free cash flows.

Author’s spreadsheet

In good years they should be able to make around $200-$300 million in free cash flows, and in a bad year, either break even or lose some money.

Lately, due to high energy and food prices combined with rising interest rates, Pakistan’s and Bangladesh’s currencies have depreciated rapidly as the trade deficits have widened, and these countries are running out of US dollar reserves. So, in the coming years, the earnings potential from those countries will likely stay low. However, VEON does have over 110 million customers in these regions, and the average monthly revenue per customer is only $1.2. Therefore, as Pakistan’s and Bangladesh’s economies develop, there is a massive long-term growth potential when the revenues per customer grow over time.

The average free cash flow yield should be around $150 million, likely growing about 4% annually in the first decade and slowing down over time. Putting it in my valuation model with a 10% discount rate, I’ll get a net present value of $3.6 billion.

Author’s valuation model

Then there is the Ukrainian business which made between $500-$700 million EBITDA before the war, and capex was only around $200 million. Corporate tax in Ukraine is 18%. The average investment cycle capex levels in Ukraine are probably higher than in previous years, but let’s say that if the situation in Ukraine returns to normal, there is potential for an additional $300 million in free cash flows.

With the additional $300 million in free cash flows but an overall slower growth rate, I get a valuation of $5.3 billion.

Author’s valuation model

There is plenty of upside compared to the current market cap of $1.2 billion.

If there is no growth and all the value in Ukraine will be permanently lost, the stock is still likely fairly priced for a 10% return.

Catalysts

There are three catalysts to unlock shareholders’ value:

1) The completion of the Russian operations sale in June. Once the market sees debt levels falling, political risks mitigated, and VEON with a reclaimed credit rating, the stock will likely get revalued.

2) When global energy and food prices fall, Pakistan’s and Bangladesh’s economies will likely stabilize.

3) The most significant catalyst is a solution for the Ukraine war.

Main risks

In the current market situation, VEON cannot get debt refinancing. If the Russian operations sales plan doesn’t go through, VEON’s liquidity balance won’t be sufficient to cover 2025 debt maturities, and VEON could face a significant default risk.

VEON’s operating markets are unstable, with high inflation, foreign exchange rate fluctuations, corruption, currency restrictions, and political risks.

The debt level will still be high after the sale process, and if VEON’s borrowing costs stay well above the return on assets, it could lead to further asset sales or even bankruptcy.

Conclusion

In my opinion, VEON is trading significantly below its intrinsic value, and multiple potential catalysts are on the horizon to unlock the value. Of course, there are significant risks, so I advocate limiting the portfolio exposure, but overall, the risk/reward is extremely positive.

{kind=link}