- Prelim was 49.3

- Prior was 47.3

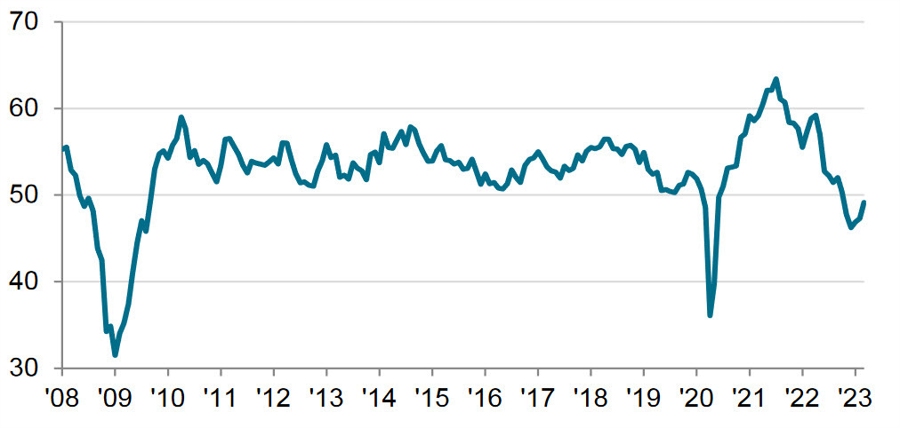

The ISM manufacturing survey is due out at the top of the hour.

Siân Jones, Senior Economist at S&P Global Market

Intelligence, said:

“The US manufacturing sector continued to signal concerning trends during March. Although output rose for the first time since last October, growth was fractional, and largely supported by ramping up production following an unprecedented reduction in supply chain pressures. The timely delivery of inputs allowed firms to work through backlogs, but sparse demand amid pressure on customer spending due to higher interest rates and inflation spoke to challenges ahead for goods producers if there is little change in domestic and international client appetite.

“Weak demand for inputs resulted in some relief for manufacturers as input cost inflation slowed again. A paucity of new orders sparked efforts to entice customers, however, as selling price inflation eased notably to the weakest since October 2020. Nonetheless, inflationary concerns weighed on business confidence once again amid pressure on margins.

“Encouragingly, firms were able to expand factory workforce capacity again, albeit at only a marginal pace, as skilled candidates for long-held vacancies were found.”

{kind=link}