As US trading session commences, rebounds of Dollar and Yen seem to be gathering a bit more some steam. The broader financial market appears to be rather listless today, with major European indices roughly flat and US futures slightly down. There’s also no unified movement in the U.S. and European benchmark treasury yields. Investors appear to be holding their bets ahead of key events tomorrow, namely UK CPI data and Fed Jerome Powell’s testimony, then BoE and SNB rate decisions the day after.

For now, Yen, Euro and Dollar are the stronger ones for the day. Australian Dollar is the worst performer after RBA minutes raised some doubts on July rate hike. Aussie is followed by Kiwi and then Sterling, in a mild risk aversion environment. Swiss Franc and Canadian Dollar are mixed.

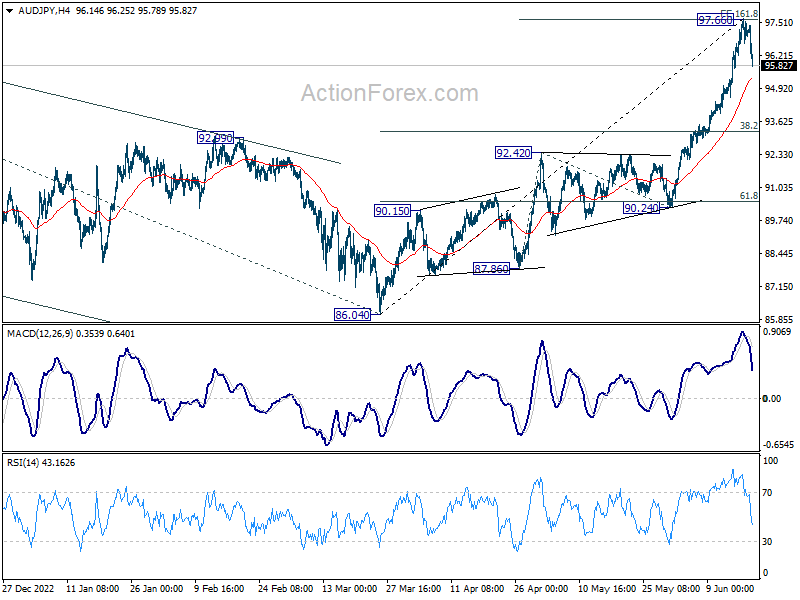

Technically, AUD/JPY should have now turn into a corrective phase with today’s pull back. The question is on whether it’s correcting the whole rise from 86.04. It’s possible that such rally has completed a five-wave sequence after meeting 161.8% projection of 87.86 to 92.42 from 90.24 at 97.61. If that’s the case, AUD/JPY could easily dive through 55 4H EMA (now at 95.27) to 38.2% retracement of 86.04 to 97.66 at 93.22. Let’s see how AUD/JPY reacts to the EMA and we’ll know quickly.

In Europe, at the time of writing, FTSE is up 0.14%. DAX is down -0.16%. CAC is up 0.11%. Germany 10-year yield is down -0.0771 at 2.442. Earlier in Asia, Nikkei rose 0.06%. Hong Kong HSI dropped -1.54%. China Shanghai SSE fell -0.47%. Singapore Strait Times lost -0.65%. Japan 10-year JGB yield declined -0.0052 to 0.390.

ECB Rehn: Inflation excluding energy and food is falling only gradually

ECB Governing Council member Olli Rehn has underscored the significance of core inflation in guiding the bank’s monetary-policy decisions. His comments comes at a time when consumer prices in eurozone are reportedly slowing, but not at the desired pace.

Rehn stated, “The rise in consumer prices in the euro area is slowing, but not to the extent desired,” further adding, “Inflation excluding energy and food is falling only gradually.”

Highlighting the primacy of core inflation – which excludes the volatile sectors of energy and food – in policy considerations, Rehn remarked, “I consider core inflation a very important, essential yardstick in the overall judgment of monetary-policy making.”

Rehn emphasized ECB’s commitment to bringing inflation back to its target, saying, “We will bring interest rates to levels sufficiently restrictive to achieve a timely return of inflation to the 2% medium-term target and keep them there as long as necessary.”

RBA minutes: Finely balanced arguments for hold and hike

Minutes from RBA’s June 6 monetary policy meeting reveal an active debate over whether to hold or raise the cash rate by 25bps.

As stated in the minutes, “Members recognised the strength of both sets of arguments, concluding that the arguments were finely balanced.” However, they ultimately determined that a rate increase was the stronger course of action at this meeting.

Recent data indicating that inflation risks had begun tilting to the upside were a key influence on the board’s decision. As they noted, “Given this shift and the already drawn-out return of inflation to target, the Board judged that a further increase in interest rates was warranted.”

Such a move would bolster confidence that inflation would indeed return to the target range “over the period ahead”, they reasoned.

At the meeting, RBA raised cash rate target by 25bps to 4.10%.

RBA Bullock: Economy needs to grow at a below trend pace for a while

In a speech, RBA Deputy Governor Michele Bullock noted the economy needs to “grow at a below trend pace for a while” to bring demand and supply into better balance. Only that will give “the greatest chance of securing sustainable full employment into the future.”

Bullock explained, “For monetary policy… We think of full employment as the point at which there is a balance between demand and supply in the labour market (and in the markets for goods and services) with inflation at the inflation target.”

“In recent months, the balance between labour demand and supply has improved somewhat,” she noted. “Nevertheless, the labour market remains tight.”

Also, “for the first time in decades, firms’ demand for labour exceeds the amount of labour that people are willing and able to

“At the same time, with demand for goods and services high relative to the economy’s capacity to supply those things, inflation is well above the 2–3 per cent target range.”

PBoC cuts two key lending rates

China’s PBoC executed cuts to two of its pivotal lending rates today, marking the first time such adjustments have been made in 10 months since last August.

The Chinese central bank opted to reduce one-year loan prime rate by -10 bps, taking it down from 3.65% to 3.55%. Concurrently, it also implemented a -10 bps cut to five-year loan prime rate, adjusting it from 4.3% to 4.2%.

These measures follow other recent actions aimed at easing monetary policy. Only last Thursday, PBOC made its first cut to one-year medium-term loan facility in 10 months. Furthermore, the bank reduced its seven-day reverse repurchase rate on the preceding Monday.

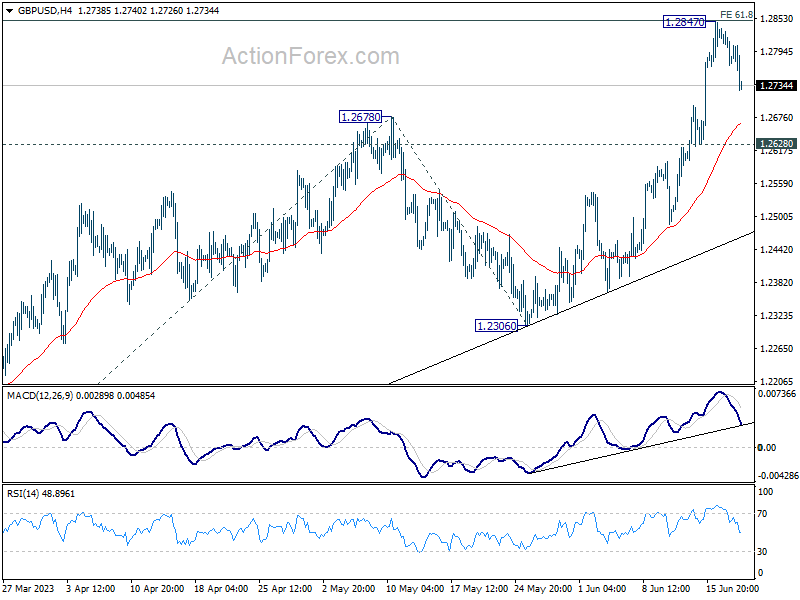

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2764; (P) 1.2801; (R1) 1.2830; More…

GBP/USD’s retreat from 1.2847 extends lower today but stays well above 1.2628 support. Intraday bias remains neutral first and further rally is expected. On the upside, firm break of 1.2847 will resume larger up trend and target 100% projection of 1.1801 to 1.2678 from 1.2306 at 1.3183 next.

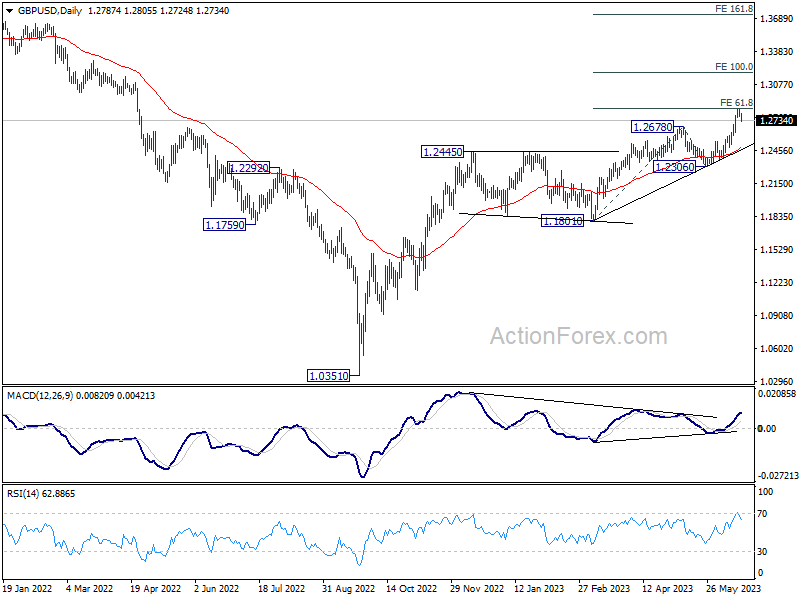

In the bigger picture, the strong support from 55 W EMA (now at 1.2345) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | RBA Minutes | ||||

| 04:30 | JPY | Industrial Production M/M Apr F | 0.70% | -0.40% | -0.40% | |

| 06:00 | CHF | Trade Balance (CHF) May | 5.48B | 3.45B | 2.60B | 2.56B |

| 06:00 | EUR | Germany PPI M/M May | -1.40% | -0.70% | 0.30% | |

| 06:00 | EUR | Germany PPI Y/Y May | 1.00% | 1.70% | 4.10% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Apr | 4B | 27.3B | 31.2B | |

| 12:30 | USD | Housing Starts May | 1.63M | 1.40M | 1.40M | 1.34M |

| 12:30 | USD | Building Permits May | 1.49M | 1.43M | 1.42M |

{kind=link}