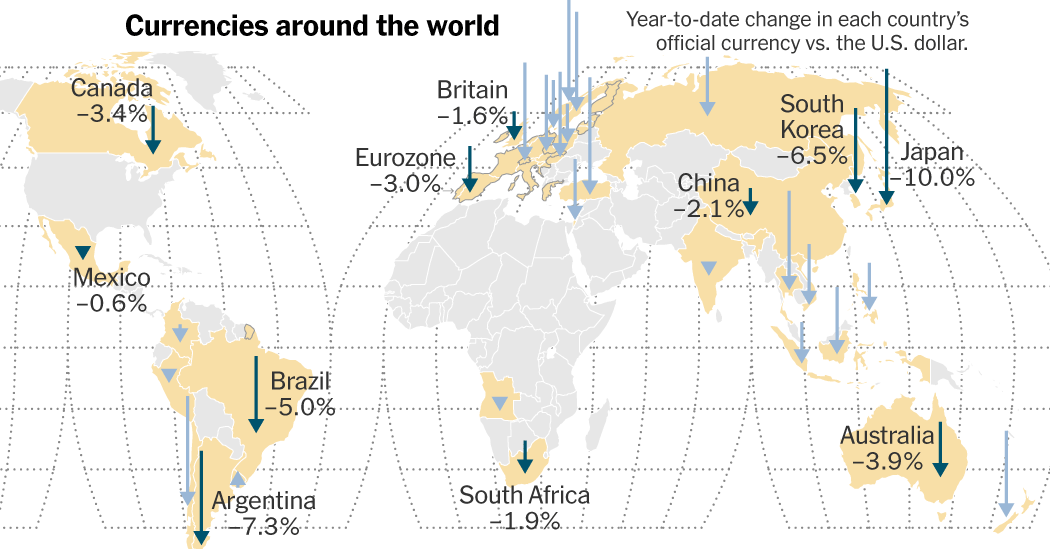

Every major currency in the world has fallen against the U.S. dollar this year, an unusually broad shift with the potential for serious consequences across the global economy.

Two-thirds of the roughly 150 currencies tracked by Bloomberg have weakened against the dollar, whose recent strength stems from a shift in expectations about when and by how much the Federal Reserve may cut its benchmark interest rate, which sits around a 20-year high.

High Fed rates, a response to stubborn inflation, mean that American assets offer better returns than much of the world, and investors need dollars to buy them. In recent months, money has flowed into the United States with a force that’s being felt by policymakers, politicians and people from Brussels to Beijing, Toronto to Tokyo.

The dollar index, a common way to gauge the general strength of the U.S. currency against a basket of its major trading partners, is hovering at levels last seen in the early 2000s (when U.S. interest rates were also similarly high).

The yen is at a 34-year low against the U.S. dollar. The euro and Canadian dollar are sagging. The Chinese yuan has shown notable signs of weakness, despite officials’ stated intent to stabilize it.

“It has never been truer that the Fed is the world’s central bank,” said Jesse Rogers, an economist at Moody’s Analytics.

When the dollar strengthens, the effects can be fast and far-reaching.

The dollar is on one side of nearly 90 percent of all foreign exchange transactions. A strengthening U.S. currency intensifies inflation abroad, as countries need to swap more of their own currencies for the same amount of dollar-denominated goods, which include imports from the United States as well as globally traded commodities, like oil, often priced in dollars. Countries that have borrowed in dollars also face higher interest bills.

There can be benefits for some foreign businesses, however. A strong dollar benefits exporters that sell to the United States, as Americans can afford to buy more foreign goods and services (including cheaper vacations). That puts American companies that sell abroad at a disadvantage, since their goods appear more expensive, and could widen the U.S. trade deficit at a time when President Biden is promoting more domestic industry.

Exactly how these positives and negatives shake out depends on why the dollar is stronger, and that depends on the reason U.S. interests rates might remain high.

Earlier in the year, unexpectedly strong U.S. growth, which can lift the global economy, had begun to outweigh worries over stubborn inflation. But if U.S. rates remain high because inflation is sticky even as economic growth slows, then the effects could be more “sinister,” said Kamakshya Trivedi, an analyst at Goldman Sachs.

In that case, policymakers would be stuck between supporting their domestic economies by cutting rates or supporting their currency by keeping them high. “We are at the cusp of that,” Mr. Trivedi said.

The strong dollar’s effects have been felt particularly sharply in Asia. This month, the finance ministers of Japan, South Korea and the United States met in Washington, and among other things they pledged to “consult closely on foreign exchange market developments.” Their post-meeting statement also noted the “serious concerns of Japan and the Republic of Korea about the recent sharp depreciation of the Japanese yen and the Korean won.”

The Korean won is the weakest it has been since 2022, and the country’s central bank governor recently called moves in the currency market “excessive.”

The yen has been tumbling against the dollar, and on Monday briefly slipped past 160 yen to the dollar for the first time since 1990. In sharp contrast to the Fed in the United States, Japan’s central bank began raising interest rates only this year after struggling for decades with low growth.

For Japanese officials, that means striking a delicate balance — increase rates, but not by too much in a way that could stifle growth. The consequence of that balancing act is a weakened currency, as rates have stayed near zero. The risk is that if the yen continues to weaken, investors and consumers may lose confidence in the Japanese economy, shifting more of their money abroad.

A similar risk looms for China, whose economy has been battered by a real estate crisis and sluggish spending at home. The country, which seeks to hold its currency within a tight range, has recently relaxed its stance and allowed the yuan to weaken, a demonstration of the pressure exerted by the dollar in financial markets and on other countries’ policy decisions.

“A weaker yuan is not a sign of strength,” said Brad Setser, a senior fellow at the Council on Foreign Relations and former Treasury Department economist. “It will lead to questions about whether China’s economy is as strong as people thought.”

In Europe, policymakers at the European Central Bank have signaled that they could cut rates at their next meeting, in June. But even with inflation improving in the eurozone, there is a concern among some that by lowering interest rates before the Fed, the E.C.B. would widen the difference in interest rates between the eurozone and the United States, further weakening the euro.

Gabriel Makhlouf, governor of Ireland’s central bank and one of the 26 members of the E.C.B.’s governing council, said that when setting policy, “we can’t ignore what’s happening in the U.S.”

Other policymakers are confronting similar complications, with central banks in South Korea and Thailand among those also considering lowering interest rates.

By contrast, Indonesia’s central bank unexpectedly raised rates last week, in part to support the country’s depreciating currency, a sign of how the dollar’s strength is reverberating around the world in different ways. Some of the fastest-falling currencies this year, like those in Egypt, Lebanon and Nigeria, reflect domestic challenges made even more daunting by the pressure exerted by a stronger dollar.

“We are on the edge of a storm,” Mr. Rogers of Moody’s said.

Eshe Nelson contributed reporting.

{kind=link}