Yesterday we had the DP Non-Farm Employment Change which came in stronger and JOLTS job openings which were weaker, ahead of the FOMC meeting. Besides that, a notable issue was the slowdown in the US manufacturing activity, with the US ISM manufacturing indicator falling below 50 points again, which means contraction.

The market was on edge ahead of the FED meeting, particularly after a strong labour earnings index on Monday, but the FOMC alleviated fears of rate hikes. Despite this, the US dollar gave back some of its gains from earlier in the week before stabilizing ahead of the announcement. The statement itself was largely uneventful, with no noticeable shifts towards hawkishness.

However, it did surprise some with a QT taper of $35 billion instead of the expected $30 billion. Later in the press conference Powell emphasized that a slight uptick in the unemployment rate would not be sufficient to warrant rate cuts. As Powell spoke, the dollar weakened across the board, but by the end of the news conference, the trend had reversed. Equities also erased all of their gains and more.

This could indicate growing doubts about the likelihood of inflation easing, or it might be driven by economic concerns. The most significant bout of dollar selling occurred as Powell resisted multiple attempts to push him towards a more hawkish stance. He reiterated that the Fed’s primary scenario involves either cutting rates or waiting longer for greater confidence in inflation easing. However, there was a fight back from USD buyers, since he didn’t commit to rate cuts either.

Today’s Market Expectations

Today we had the Switzerland Consumer Price Index (CPI) Month-over-Month (M/M) which was anticipated to show a 0.1% increase, compared to the previous reading of 0.0%. However, there’s no consensus available yet on the Year-over-Year (Y/Y) measure. In the previous release, the data missed expectations once again, dropping to 1.0% versus an anticipated 1.3%. Given that the market has already factored in a rate cut in June and for the remainder of the year, another significant decline might prompt an adjustment in the scale of the cuts from 25 basis points (bps) to 50 bps.

The US Jobless Claims report which will be released later remains highly significant on a weekly basis as it offers a timely indication of the labor market’s condition. This is crucial because a weakening labor market raises the likelihood of falling short of the Fed’s inflation target. Conversely, a resilient job market may pose challenges in meeting the target. Initial Claims have been hovering near their lowest levels in the current economic cycle, while Continuing Claims have remained steady around the 1800K mark. For this week, Initial Claims are expected to be 212K compared to 207K previously, while there’s no consensus on Continuing Claims yet, given the previous announcement showed a decline to 1781K versus an expected 1814K and 1796K in the prior period.

Yesterday the volatility picked up in the US session after being low in the European session. We had some mixed employment figures from the US, while ISM manufacturing fell into contraction. We didn’t open any forex signals since the market could go either way during the FOMC meeting, so we just opened two forex signals, both of which closed in profit.

Gold Climbs Back Above $2,300

GOLD prices had been consolidating above $2,300 for several days after dropping below $2,400. Buyers managed to maintain prices within a range, fluctuating between $2,310 and $2,350. However, XAU resumed its decline, falling below $2,300. Calmer geopolitical tensions have improved risk sentiment in financial markets, leading to a decrease in demand Gold. However, yesterday, gold prices moved back above $2,300 following the FOMC meeting.

XAU/USD – Daily chart

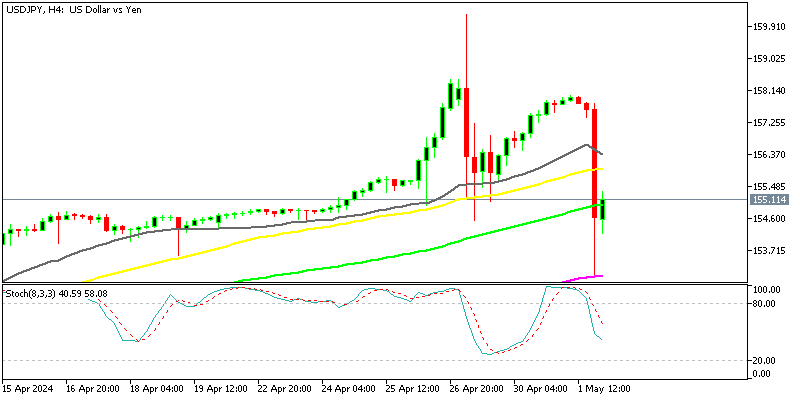

Enormous Volatility in USD/JPY After Another BOJ Intervention

After the FED meeting yesterday evening, they intervened once more, likely capitalizing on the liquidity, which led to USD/JPY dropping below 155. Japanese officials stepped in again, this time right after the US market closed. Their intervention caused USD/JPY to fall below both the 50- and 100-day moving averages. The price continued to decline, breaking through the moving averages and reaching a low of 153.00. But, the price bounced off the 200 SMA and ended the day above 155.

Cryptocurrency Update

Buying the Dip in Bitcoin at the 100 Daily SMA

Bitcoin has fallen below the $60,000 mark after bouncing back to $68,000, following the first dip below this level. Currently, BTC is trading below the 100 Simple Moving Average (SMA) (green line). We are looking to buy this retreat in BTC/USD though, expecting the Bitcoin price to move back up toward 470,000.

Ethereum Stuck Between 2 MAs

Last week, Ethereum dropped below $3,000, breaching the 100-day Simple Moving Average (SMA) on the daily chart. Yet, it managed to rebound and surged above $3,000. Although buyers made significant gains, the upward momentum halted near the 50-day SMA (yellow line) and reversed direction. The 100 SMA (green) was broken this week, however the price did not fall too far from it and is staying close.

{kind=link}