(Bloomberg) — Japan is threatening to derail one of the most profitable currency bets this year: carry trades borrowing the yen to invest in emerging-market currencies.

Most Read from Bloomberg

A gauge of yen volatility jumped to the highest level since July this week as Japanese officials were suspected to have twice intervened to prop up the besieged currency. Yen-funded emerging-market carry trades are headed for a loss this week, with those targeting the Indian rupee and Colombian peso suffering among the biggest declines.

Carry trades involve investors borrowing in low-yielding currencies, such as the yen, and investing in higher-yielding ones, typically in emerging markets. The yen’s prolonged weakness and relatively low volatility have made it the premier source of borrowing this year: carry trades funded in the currency have generated positive returns versus every single emerging-market target.

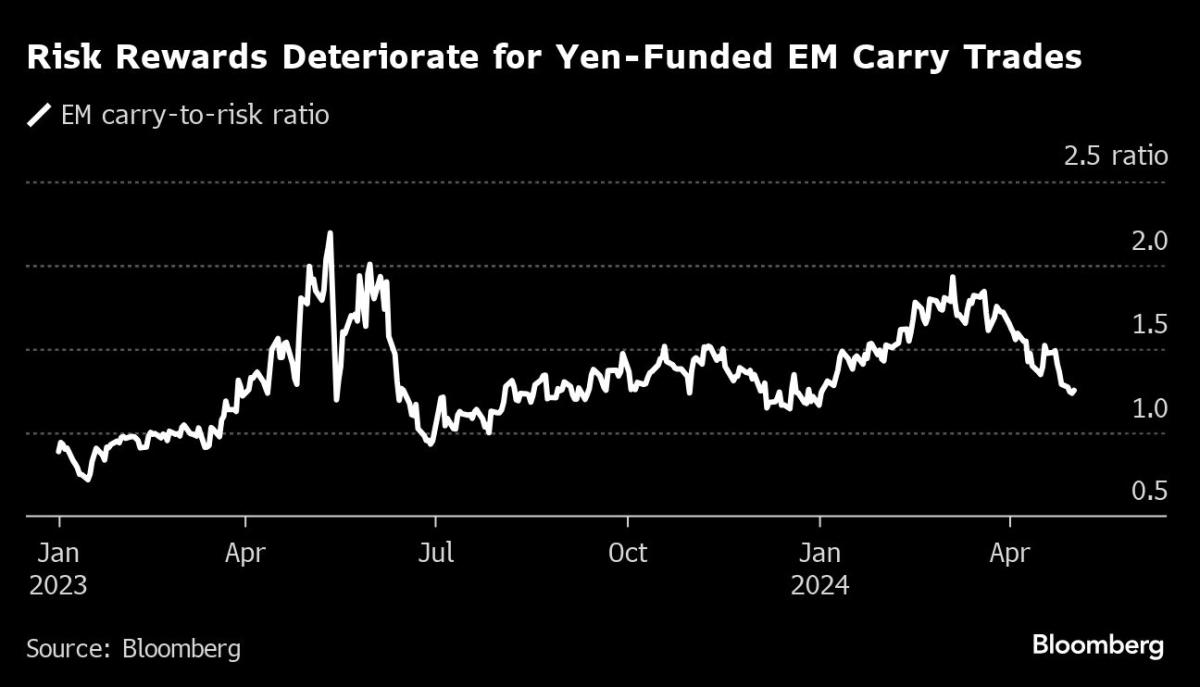

That may be about to end. The carry-to-risk ratio for yen-funded carry trades targeting eight emerging-market currencies has fallen from their highs reached in March, suggesting the risk-reward for the strategy has worsened, according to data compiled by Bloomberg. The deterioration has been mainly driven by a rise in yen volatility amid suspected intervention by the authorities, the data show.

The effect of Japan’s suspected currency intervention on emerging markets “is going to be fun to watch,” said Bob Savage, head of markets strategy and insights at BNY Mellon in New York. Investors are likely to rotate toward Asian currencies such as the Indonesian rupiah and away from the Turkish lira and the Brazilian real, he said.

The carry trade has been coming under pressure this year as the winding back of bets on Federal Reserve interest-rate cuts and rising geopolitical tensions in the Middle East sap risk appetite. The currencies of Mexico, Colombia and Argentina have all slumped more than 2% in the past month as carry traders unwound long positions due to rising funding costs and escalating volatility.

“Latam has been the destination for carry trades, so regional currencies could be most affected if yen strength does result in a bit more of a disruption,” said Brendan McKenna, an emerging-markets currency strategist at Wells Fargo in New York. “But carry trades had unwound a decent amount over the last few weeks so the impact may not be as large as it could have been, say, in early April or late March.”

To be sure, traders are skeptical the Japanese authorities will be able to prevent yen from sliding for long, as the yawning interest-rate gap between Japan and the US will likely keep it under pressures. The currency’s top forecaster expects it will weaken to 165 per dollar, a level last seen in 1986. The yen traded around 153.42 per dollar in early Asia.

For now, the yen still remains a cheap source of funding, with its forward-implied yields remaining below zero, whereas those on 30 other currencies tracked by Bloomberg are all above 1.2%. That suggests yen-funded carry trades are set to remain more attractive than possible alternatives such as borrowing the Chinese yuan.

The prospect of the emerging-market carry trade being derailed by a surge in the yen isn’t likely, said Brad Bechtel, head of global foreign exchange at Jefferies LLC in New York. “It will likely bounce back.”

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

{kind=link}