A graphic that displays the dollar performance against other currencies reveals that economic developments had mixed results on currency exchanges. The third quarter of 2023 marked a period of disinflation in the euro area, while China’s projected growth was projected to go up. The United States economy was said to have a relatively strong performance in Q3 2023, although growing capital market interest rate and the resumption of student loan repayments might dampen this growth at the end of 2023.

A relatively weak Japanese yen

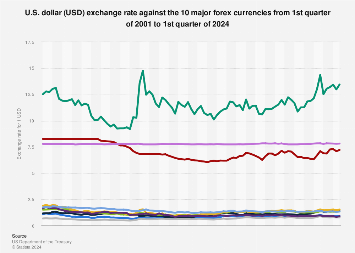

Q3 2023 saw pressure from investors towards Japanese authorities on how they would respond to the situation surrounding the Japanese yen. The USD/JPY rate was close to 150, whereas analysts suspected it should be around 90 given the country’s purchase power parity. The main reason for this disparity is said to be the differences in central bank interest rates between the United States, the euro area, and Japan. Any future aggressive changes from, especially the U.S. Fed might lower those differences. Financial markets responded somewhat disappoint when Japan did not announce major plans to tackle the situation.

Potential rent decreases in 2024

Central bank rates peak in 2023, although it is expected that some of these will decline in early 2024. That said, analysts expect overall policies will remain restrictive. For example, the Bank of England’s interest rate remained unchanged at 5.25 percent in Q3 2023. It is believed the United Kingdom’s central bank will ease its interest rate in 2024 but less than either the U.S. Fed or the European Central Bank. This should be a positive development for the pound compared to either the euro or the dollar.

{kind=link}